TMTB Morning Wrap

Good morning. Futures +20bps. Stocks in Asia mixed overnight: TPX -1.18%, NKY -0.58%, Hang Seng -0.33%, HSCEI -0.97%, SHCOMP -0.22%, Shenzhen -0.23%, Taiwan TAIEX -0.16%, Korea KOSPI -0.8%…BTC -25bps

TRUMP: YOU’RE JUST ALL HAPPY BECAUSE THE STOCK MARKET HIT AN ALL-TIME HIGH.

Jensen in DC today with GTC keynote at noon est

“Congratulate”…? (NVDA 1w call vols were bid 11v yesterday h/t MBS)

We’ll hit Earnings first then onto the usual…

EARNINGS

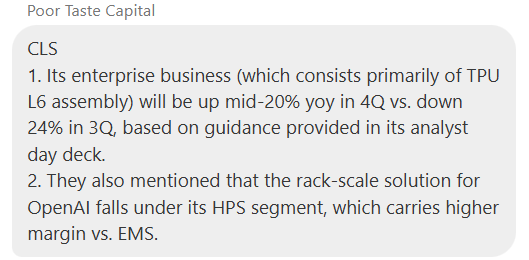

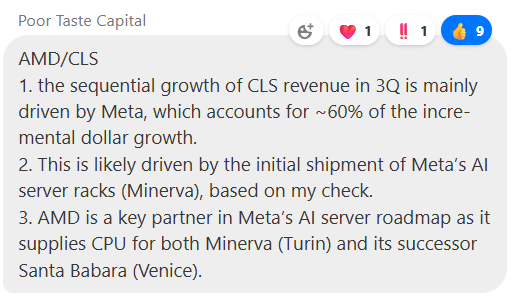

CLS +11%: Clean beat/raise with a much better F26 guide

Initial FY26 guide stole the show: $16B revenue / $8.20 EPS / 7.8% OM / $500M FCF well ahead of street and buyside which was closer to $15B / $8. Management said the demand outlook from largest customers remains strong… with indications continuing into 2027. Analyst day today…

#s Details

Q3:

Revenue $3.194B, +28% y/y (last q +21% y/y) vs Street ~$3.011B, +~20.5%

EPS (non‑GAAP) $1.58 vs Street $1.47;

Non‑GAAP OM 7.6% vs 7.5%;

Q3 CCS +43% y/y, with Communications +82% y/y (800G outpacing 400G) and HPS +79% y/y; Enterprise ‑24% y/y on a well‑telegraphed product transition (expected to flip to y/y growth from Q4 as ramps lap).

Q4’25 Guidance:

Revenue $3.325B–$3.575B (mid $3.45B, ~+36% y/y) vs Street $3.08B

EPS (non‑GAAP) $1.65–$1.81 (mid $1.73) vs Street $1.50

Non‑GAAP OM 7.6% vs Street 7.5%.

FY’25 Guidance (updated):

Revenue $12.2B, +26% y/y vs Street $11.633B.

EPS (non‑GAAP) $5.90 vs Street $5.58.

Non‑GAAP OM 7.4% vs Street 7.4%

FCF (non‑GAAP) $425M vs Street $377M

FY’26 Outlook (new):

Revenue $16.0B, +31% y/y vs Street $14.3B

EPS (non‑GAAP) $8.20 vs Street $7.13.

Non‑GAAP OM 7.8% vs Street 7.6%.

FCF (non‑GAAP) $500M vs Street $490M.

Bull vs. Bear Debate

Bulls argue CLS is becoming a structurally higher‑quality earnings compounder as hyperscalers consolidate onto a few high‑velocity partners for AI data‑center hardware (switches, storage and server programs), with Celestica’s HPS/ODM platform carrying double‑digit margins and deepening customer entanglement. They point to Q3’s mix‑driven OM high, a Q4 guide far ahead of consensus, and a FY26 reset meaningfully above buy‑side bogeys, with management signaling demand strength into 2027. Specifically, CLS is one of the best ways to gain exposure to TPU upside, META’s MTIA, and OAI. Bulls sketch $10+ 2026 EPS / $13+ in ‘27 if management’s conservative bias (typically beat initial guide by 30%) and incremental programs (e.g., large language model customers) materialize. On that math, bulls see a premium multiple versus EMS peers as warranted given scarcity value in AI infrastructure—e.g., 30-35× on $13 ~$400+

Bears counter that results are increasingly concentration‑driven (three customers at 59% of sales) and program‑specific, making the story vulnerable to design rotations, pricing resets, or timing slippage; Q3 also showed the flip side—Enterprise ‑24% y/y during a transition. They caution that sector capacity and competitor aggression (EMS/ODM peers) could compress margins once the current 800G/AI build normalizes, and question durability of 7.8% OM. On valuation, bears argue CLS already embeds a rich scarcity premium: applying a more normalized 18–22× multiple to $10EPS yields ~$200, implying downside if AI hardware growth decelerates or if mix moderates.

Positive AMD read-through:

CDNS -2% looks solid with a beat on revenue/EPS and margins, raised FY25, $7B backlog—driven by hardware momentum and a sharp China rebound.

Mgmt sounded pretty positive on the call with commentary on how AI infra has accelerated materially in the past 2 quarters and that this pillar is enabling growth across EDA, IP and Simulation. They also talked positively around displacements in IP and EDA which point to market share gains.

#s Details:

FQ3’25:

Revenue $1.339B, +10.1% y/y (last q 20.2% y/y) vs Street $1.323B, +~8.6%

EPS (non‑GAAP) $1.93 vs Street $1.79

Non‑GAAP OM 47.6% vs Street 45.5%

Backlog (RPO) $7.0B vs Street $6.75B

China mix ~18% of revenue (vs. ~13% FY24)

FQ4’25 Guidance:

Revenue $1.405–$1.435B ( ~+3.6% y/y at low end) vs Street ~$1.405B; midpoint $1.420B

EPS (non‑GAAP) $1.88–$1.94 (midpoint $1.91) vs Street $1.92

Non‑GAAP OM 44.5–45.5% (midpoint 45.0%) vs Street 46.0%

FY25 Guidance (raised):

Revenue $5.262–$5.292B (+13.7% y/y) vs Street $5.246B

EPS (non‑GAAP) $7.02–$7.08 vs Street $6.92

Non‑GAAP OM 43.9–44.9% vs Street ~44.0%

Operating Cash Flow $1.65–$1.75B vs Street ~$1.69B

Bull vs. Bear Debate

Bulls argue CDNS is one of the clearest secular winners from AI‑driven design complexity, with durable double‑digit growth anchored by a high‑visibility recurring model and an increasingly strategic hardware franchise (Palladium/Protium) that is now “annual” at top accounts. The record $7B backlog, raised FY25 guide, and management’s view that hardware revenue will be higher in 2026 support a multi‑year up‑and‑to‑the‑right narrative. IP momentum (HBM4/DDR5; faster‑growing than corporate average) and expansion into SDA via Hexagon/MSC broaden TAM and cross‑sell, while AI‑for‑design (Cerebrus/SimAI/agentic tools) creates incremental monetization vectors as contracts refresh. On valuation, bulls see low‑to‑mid‑teens top‑line and 45%+ non‑GAAP OM sustaining the multiple; Bulls say assume ~12–14% sales CAGR through CY27 (AI/hardware/IP mix), incremental margins ~45%, and apply 50–55x CY26 EPS given scarcity value and cash‑flow quality—$400+

Bears focus on valuation and mix risk: 2025 outperformance is disproportionately tied to hardware and China, both lumpier and less forecastable; recurring growth has slowed to single‑digits this year for the first time since 2020, raising questions on the core EDA cadence. Near term, Q4 OM sits below Street, SDA’s contract transition could be a drag, and regulatory/tariff risks remain a constant overhang given China exposure. If growth normalizes closer to ~11% y/y (ex‑M&A) and hardware decelerates against tough comps, a de‑rating to ~40x CY26 P/E on ~$8 EPS gets you closer to ~$315–$325.

CFLT +10%: Clean beat/raise with NRR steady at 114%, Cloud +24% y/y, non‑GAAP OM 9.7%, and solid 20% y/y Cloud guide despite AI‑native customer transition; Flink +70% q/q and late‑stage pipeline +40% q/q again

Key Takeaways:

Management characterized optimization as “normalized…healthy”

Flink ARR for Confluent Cloud grew >70% q/q, now 1,000+ customers, with a low‑8 figure ARR comment in Q&A

Late‑stage pipeline +>40% q/q (again) and RPO +43% y/y / cRPO +27% y/y increased coverage and visibility to consumption.

Management cited win rates well above 90%, average deal size doubling in the last two quarters, multi‑tenant offerings (Freight, Enterprise, WarpStream) driving a 4x consumption lift, and WarpStream consumption 8x since acquisition—also a tailwind to subscription GM over time.

International revenue grew 29% y/y vs 13% y/y in the U.S., pointing to strength outside the U.S. and Platform‑led larger deals

The Cloud→Platform move (called out last quarter) did not impact Q3, is a LSD% headwind to Q4 Cloud y/y growth, and Cloud growth would be flattish ex‑this impact

#s DETAILS:

Q3

Revenue $298.5M, +19% y/y (last q ~20% y/y) vs Street $292.9M, +~17%;

Subscription revenue $286.3M, +19% y/y (last q ~20.5% y/y) vs Street $281.6M.

Confluent Cloud revenue $161.0M, +24% y/y (last q ~28% y/y) vs Street $157.9M.

Confluent Platform revenue $125.4M, +14% y/y (last q ~12% y/y) vs Street $123.7M.

EPS (Non‑GAAP) $0.13 vs Street $0.10.

Non‑GAAP OM 9.7% vs Street 7.1%.

NRR 114% (stable vs 114% last q).

RPO growth +43% y/y; cRPO +27% y/y (Q2: +31% and +21%).

Non‑GAAP GM 78.2% (subscription GM 81.8%) vs Street 78.5%.

FQ4’25 Guidance:

Subscription revenue $295.5–$296.5M, +~18% y/y vs Street $295.0M.

Confluent Cloud revenue ~$165M, +~20% y/y (flattish ex‑AI‑cust. vs Q3’s 24%) vs Street $162.7M.

Confluent Platform revenue $130.5–$131.5M, +~16% y/y vs Street $132.2M.

EPS (Non‑GAAP) $0.09–$0.10 vs Street $0.09.

Non‑GAAP OM ~7% vs Street 6.8%.

FY25 (updated):

Subscription revenue $1.1135–$1.1145B, +~21% y/y vs Street $1.109B.

EPS (Non‑GAAP) $0.39–$0.40 vs Street $0.36.

Non‑GAAP OM ~7% vs Street 6.2%.

Bull vs. Bear Debate

Bulls argue Confluent is emerging as the de‑facto streaming and context layer for AI‑era applications, with structural share gains vs. hyperscalers and open source. Management called out >90% win rates against CSP streaming offerings, doubling deal sizes in the last two quarters, and multi‑tenant offerings (Freight/Enterprise/WarpStream) that lift consumption 4x and should be a gross‑margin tailwind over time. Add two straight quarters of >40% q/q late‑stage pipeline growth, RPO +43% y/y, and Flink >70% q/q (1,000+ customers) and bulls see strengthening leading indicators plus better execution (field alignment, DSP specialists). They view the Q4 Cloud headwind from one AI‑native customer as idiosyncratic and already quantified, with “flattish” growth ex‑impact, setting up for 2026 acceleration. A potential bid at 7x could reach high 20s.

Bears focus on the consumption model’s variability and the risk that optimizations recur or that net‑new use cases fail to scale quickly, especially among smaller customers where net adds remained weak. They also highlight Cloud growth deceleration (to ~24% y/y) and the dependency on larger cohorts (>$100k/$1M) while the <$100k bucket lags, raising questions on the pipeline‑to‑revenue conversion and broader demand elasticity in a still‑mixed IT spend environment. Competitive risks from AWS/Azure/GCP managed Kafka/Flink offerings persist; while win rates are high today, hyperscalers’ bundled pricing and native integration could pressure pricing/mix. Finally, Flink is still small (low‑8 figures) and may take time to materially move the needle. Bears argue for something closer to 5x sales which is low 20s

Earnings Quick hits:

W +9% with a beat as revenue came in at $3.12B vs. $3.01B consensus, with EBITDA of $208M vs. $163.8M expected. Orders exceeded estimates at 9.8M vs. 9.36M, though ending active customers were slightly below at 21.2M vs. 21.46M.

CHKP +10% with a big billings beat ($672M vs street at $607M) growing close to 20%. Total revenue also grew 7% Y/Y to narrowly beat consensus. Non-GAAP EPS of $3.94 easily beat street $2.45, but this was largely due to a one-time tax benefit of $1.47, as operating margins slightly missed targets. Cash flow from operations remained strong, also beating expectations despite a one-time tax payment. Growth was attributed to demand for its hybrid mesh network, Workspace, and External Risk Management (ERM) solutions.

GLW -8%: Smaller than expected beat and raise missed high expectations. 1% rev beat Q3 revenue/operating Margin/EPS of $4.27b/19.6%/$0.67 vs. Street at $4.24b/20.1%/$0.66. Q4 revenue/EPS guidance of $4.35b/$0.70 vs. Street at $4.29b/$0.68

PYPL +17% after announcing ChatGPT deal. Quarter was ok as TMS beat by 2.5% despite higher txn losses from German outage and q end commentary which signals low end of 3-5% range. Upside due to OVAS + lower credit losses. Branded +5%. Q4 TMS guide slightly below at 2-5% vs street at 4%.

PayPal signs deal with OpenAI to become the first payments wallet in ChatGPT

CNBC:

PayPal has signed a deal with OpenAI to have its digital wallet embedded into ChatGPT so users can pay for items found through the leading consumer AI tool, the company told CNBC exclusively.

The agreement, sealed over the weekend, means that starting next year, both sides of PayPal’s ecosystem can plug into ChatGPT: PayPal users can purchase items through the AI platform, and its merchants can sell on it, with their inventory listed there, according to PayPal CEO Alex Chriss.

“We’ve got hundreds of millions of loyal PayPal wallet holders who now will be able to click the ‘Buy with PayPal button’ on ChatGPT and have a safe and secure checkout experience,” Chriss said in an interview.

TECH RESEARCH/NEWS

AMZN: Comments on Job Cuts in blog post - 14k less than 30k in reports yesterday

While this will include reducing in some areas and hiring in others, it will mean an overall reduction in our corporate workforce of approximately 14,000 roles. We’re working hard to support everyone whose role is impacted, including offering most employees 90 days to look for a new role internally (the timing will vary some based on local laws), and our recruiting teams will prioritize internal candidates to help as many people as possible find new roles within Amazon. For our teammates who are unable to find a new role at Amazon or who choose not to look for one, we’ll offer them transition support including severance pay, outplacement services, health insurance benefits, and more.

Looking ahead to 2026, as Andy talked about earlier this year, we expect to continue hiring in key strategic areas while also finding additional places we can remove layers, increase ownership, and realize efficiency gains.