TMTB Morning Wrap

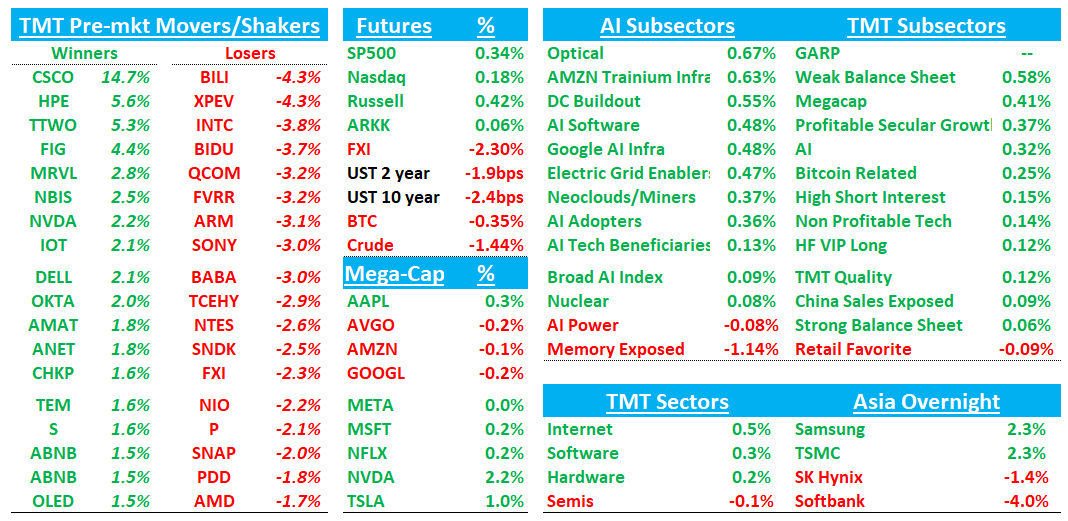

Good morning. Futures +30bps to start the day. Oil -1%. BTC flat.

All eyes on the Trump-Xi summit over the next couple of days.

Asia Mixed overnight: Korea +175bps, India +118bps, Taiwan +91bps, HK flat, Japan -98bps, China -152bps.

In tech, hardware/networking rallying on the back of CSCO’s big AI number while CPU/memory weaker.

We’ll hit CSCO Earnings first, then get to the usual…

Let’s get straight to it…

CSCO: Clean beat-and-raise, but more important huge step-function AI order guide, stronger non-AI/networking orders, and a materially above-Street FQ4 guide.

Sentiment/positioning leaned bullish here, but the guide and AI # were much better than expects and strengthens the narrative of CSOC as a “cheap” AI winner.

Other networking names up in the pre: HPE +6%/ANET +2%/MRVL 4%+. Scale across wins read through positive to NOK +5%.

The #s:

Revenue was $15.841B, +12.0% y/y (last q +9.7% y/y) vs Street ~$15.54B, +~9.9%; non-GAAP EPS was $1.06 vs Street ~$1.03-$1.04.

FQ4 revenue guide of $16.7-$16.9B, +~14.5% y/y at the midpoint, was far above Street ~$15.8B, +~7.8%; EPS guide of $1.16-$1.18 was also well above Street ~$1.07-$1.08.

Product orders were +35% y/y, ex-hyperscaler +19% y/y, and AI infrastructure orders from hyperscalers were $1.9B in FQ3, taking YTD to $5.3B and causing mgmt to raise FY26 AI orders to ~$9B from the prior ~$5B.

Key Takeaways:

AI hyperscaler orders were $1.9B in FQ3, YTD orders reached $5.3B, and FY26 AI order expectations were raised to ~$9B from ~$5B. FY26 AI revenue was raised to ~$4B from ~$3B, and mgmt pointed to at least ~$6B of FY27 AI hyperscaler revenue. The AI mix was roughly split between Silicon One systems and Acacia optics, with five hyperscaler design wins in FQ3, including P200 scale-across and G200 scale-out wins

The non-AI/networking part of the story also improved: Total product orders grew +35% y/y and +19% y/y ex-hyperscalers, with Enterprise +18%, Public Sector +27%, SP/Cloud +105%, and networking product orders +50%+. Campus orders were +25%, data center switching orders +40%+, wireless orders +40%+, and mgmt framed enterprise AI inference/agentic workloads as a driver of private data center and campus modernization.

Mgmt acknowledged some pull-forward was reasonable to assume, but called it “very modest,” noting that 4-5 points of the 9-point acceleration in ex-webscale orders came from price, not units, and that the FQ4 pipeline showed no degradation through FQ3. Bears will still argue the 35% product order print looks partly like customers getting ahead of pricing and component availability

Non-GAAP GM was 66.0%, down 260 bps y/y and 150 bps q/q, with product GM down 330 bps y/y due to mix and higher memory costs. FQ4 GM guide of 65.5%-66.5% was below some Street expectations, but mgmt said GMs have stabilized, aided by pricing, memory-utilization programs, DDR4-to-DDR5 conversions, and advanced purchase commitments.

Mgmt emphasized in-house Silicon One control, secured silicon supply through CY26, a Nanya supply agreement, $6.7B of incremental inventory/advanced purchase commitments over the last 90 days, and no supplier decommits.