TMTB Morning Wrap

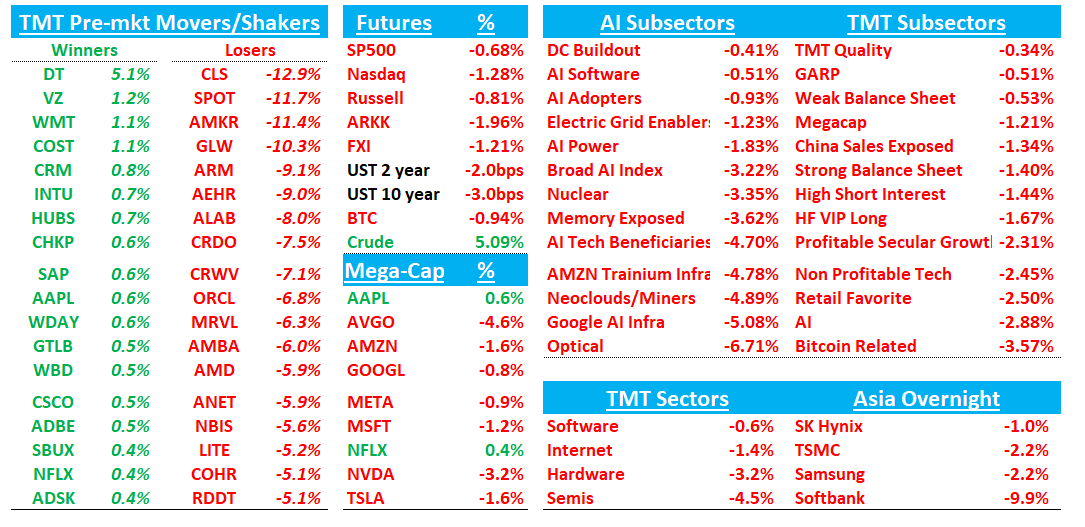

Good morning. Futures -1.25% as a WSJ article calling out OAI missing internal targets last year & Q1 revenue targets hitting semis early, with the group down 4%+.

Key quote from WSJ:

Board of directors have also more closely examined the company’s data-center deals in recent months and questioned Chief Executive Sam Altman’s efforts to secure even more computing power despite the business slowdown, the people said.

The spending scrutiny is constraining Altman’s once-boundless ambitions ahead of a potential initial public offering that could take place by the end of the year. Friar and other executives are now seeking to control costs and instill more discipline in the business, at times putting them at odds with their CEO.

A lot of this does seem backward looking and before OAI pivoted to enterprise and the Codex ramp, but with Oil +5% encouraging a risk off morning, semis having had a huge run MTD, froth reading near highs, along with some weaker earnings from RMBS/CLS, all combining to have the group down early. OAI complex getting hit the most: Softbank was down 10% overnight. ORCL -8%. AMD -6%. CRWV -7% NVDA -3% although MSFT -1% hanging in fine (I guess severing some ties with OAI yesterday now works in their favor ;) ). Good discussion in TMTB Slack here on the news.

Asia mostly saw losses, but there were a few pockets of green: TPX +0.99%, NKY -1.02%, Hang Seng -0.95%, HSCEI -1.27%, SHCOMP -0.19%, Shenzhen -1.07%, Taiwan TAIEX -0.24%, Korea KOSPI +0.39%.

We’ll cover SPOT, CDNS, RMBS, and CLS first, then onto the usual.

Let’s get to it…

SPOT -10%: Not enough as Q1/Q2 Premium subs miss and OI guided lower

Call ongoing…

The Prem miss will likely embolden bears who will were already saying sub growth was saturated and will point to elevated churn as being evidence of a mature weighted product. Now you have a heavily weighted 2H guide with limited visibility. Other nits here: advertising missed (biddable ads creating ST headwind for LT gain)and OI guide is weaker — mgmt had kind of telegraphed lower OI increase in 2H of the year, but this again will have bears pointing to a step function higher in AI-related expenses (and fears around competitive environment increasing).

1Q Premium Subscriber Adds: 3M vs bogey 4M vs guide 3M

2Q Premium Subscriber Add Guide: 6M vs bogey 6M vs Street 7.5M

1Q Revenue: EUR 4.5B vs bogey EUR 4.6B vs guide EUR 4.5B

2Q Revenue Guide: EUR 4.8B vs bogey EUR 4.8B

1Q OI: 715M vs bogey 715M

2Q OI Guide: 630M vs bogey 700M+

1Q GM: 33% vs bogey 33%+ vs guide 32.8%

2Q GM: 33.1% vs bogey/street 33.1%

CDNS -2%: Clean beat-and-raise, but the stock debate remains whether agentic AI changes the EDA growth curve rather than whether Q1 was good.

The #s:

1Q Revenue was $1.474B, +18.7% y/y (last q +6.2% y/y) vs Street $1.450B, +~17%; EPS was $1.96 vs Street $1.88; non-GAAP OM was 44.7% vs Street 44.0%. Bookings ahead with record backlog of $8B vs. $7.8B ;last q

Q2 guidance was meaningfully above Street: revenue midpoint $1.575B, +23.5% y/y vs Street $1.491B, +~17%, EPS midpoint $2.05 vs Street $1.84, and non-GAAP OM midpoint 45.0% vs Street 42.7%.

FY26 revenue guide moved to $6.125-6.225B, midpoint $6.175B, +16.6% y/y vs Street $6.132B, +15.8%, with $160M from Hexagon and a $65M organic raise; FY26 EPS guide went down optically to $7.85-7.95 due to $0.28 Hexagon dilution, but organic EPS was raised $0.08.

Key Takeaways:

Mgmt positioned AgentStack, ChipStack, ViraStack and InnoStack as a new product category, not just feature upgrades. The key investor point is two-fold: new subscription-plus-consumption revenue from agentic tools, plus higher base-tool consumption as agents run more simulations, verification and optimization loops.

Pricing: Mgmt said the pricing environment improved, tied agentic AI value capture to customer productivity, and framed labor-to-automation spend shifts as “likely to be irreversible.” This matters because one long-standing bear critique of EDA has been that large customers capture too much of the value through volume discounts.

Demand/Macro: Mgmt said the environment is healthy across system companies and semi companies, with hyperscalers and AI semi already strong and memory plus analog/mixed-signal improving over the last 3-6 months. Chip shortages are not restricting design activity in their view; if anything, customers may design across multiple foundries/nodes to secure capacity, which drives more design activity.

Mgmt said hardware had its best quarter ever, led by AI/HPC with rising automotive and robotics demand. Palladium Z3 drove competitive displacements, and mgmt argued its ASIC-based hardware lead should widen versus FPGA-based alternatives.

Mgmt described IP as entering a third year of strong growth, helped by better PPA, expanding portfolio breadth in HBM/UCIe and other interface/memory IP, and foundry proliferation. The large foundry deal was not Intel; mgmt nevertheless sounded positive on Intel 18A and especially 14A enablement.

Hexagon is a near-term EPS/OM headwind, but bulls see physical AI optionality. FY26 includes ~$160M of Hexagon revenue, a 5-10% margin profile, and ~$0.28 EPS dilution from integration and financing effects. Mgmt expects accretion in 2027, likening the integration path to BETA CAE.

Bull vs. Bear Debate

Bulls think CDNS is one of the cleanest picks-and-shovels beneficiaries of AI silicon complexity. The traditional bull case is that EDA is mission-critical, sticky, consolidated among a small number of vendors, and levered to long-duration semi R&D rather than near-term chip unit volatility. This quarter strengthened that case because bookings were ahead of expectations, backlog reached a record $8B, hardware demand accelerated, and the company raised FY26 revenue organically by $65M after only one quarter. Bulls also like that mgmt said EDA’s share of customer R&D has already moved from ~7% historically to ~11%, and that agentic AI could push that higher as customers try to solve the engineering talent bottleneck with more automation.

The more aggressive bull case is that agentic AI creates a new EDA monetization layer. CDNS is not just adding AI features to existing tools; it is selling new products for previously manual work like RTL generation, verification planning, analog design and implementation. The most important change is that these tools can be priced with subscription-plus-consumption while also increasing usage of the underlying base tools. Bulls also point to physical AI and Hexagon as a second TAM expansion path: simulation for robotics, autonomous systems, cars and 3D-IC, plus more silicon design as physical AI proliferates.

On valuation/growth, bulls generally underwrite CDNS as a mid-teens compounder with upside if agentic AI moves monetization faster than the normal contract-cycle cadence. A reasonable bull path is FY26 revenue growth of ~16-17% including Hexagon, FY27 growth in the mid-teens if hardware, IP, agentic AI add-ons and SD&A momentum continue, and EPS reaccelerating toward high-teens/20% growth once Hexagon dilution flips to accretion. At 40x EPS of $9.5, you get a $400+ stock. That valuation is rich, but bulls argue it is justified if agentic AI raises long-term EDA growth from low/mid-teens toward a structurally higher consumption model.

Bears agree Q1 was strong, but they argue it does not yet prove the agentic AI upside is in the numbers. The reported FY26 revenue raise included $160M from Hexagon, while the organic raise was closer to $65M. FY26 EPS guidance was cut by $0.20 at the midpoint because Hexagon is dilutive in year one, and FY26 OM guidance moved down. Bears also point out that upfront revenue grew much faster than recurring revenue, which makes current growth feel more hardware/upfront-weighted than pure recurring software. That matters because the stock trades like a scarce, high-quality software compounder.

The deeper bear case is that AI is not obviously only a benefit. Bears worry that hyperscalers, semi customers or startups could use AI to reduce dependence on incumbent EDA workflows over time, or that CDNS will have to invest heavily to defend its moat. Mgmt directly pushed back on this, but bears will want proof in renewals, attach rates and sustained organic growth. The other bear issues are familiar: China/export-control and tariff risk, hardware supply constraints, gross margin pressure from hardware and acquisitions, SBC/amortization exclusions, and a valuation that leaves little room for disappointment. On valuation, bears will say 40x is very expensive and if CDNS is not clearly an AI growth stock, the current multiple is even more difficult to defend