TMTB Morning Wrap

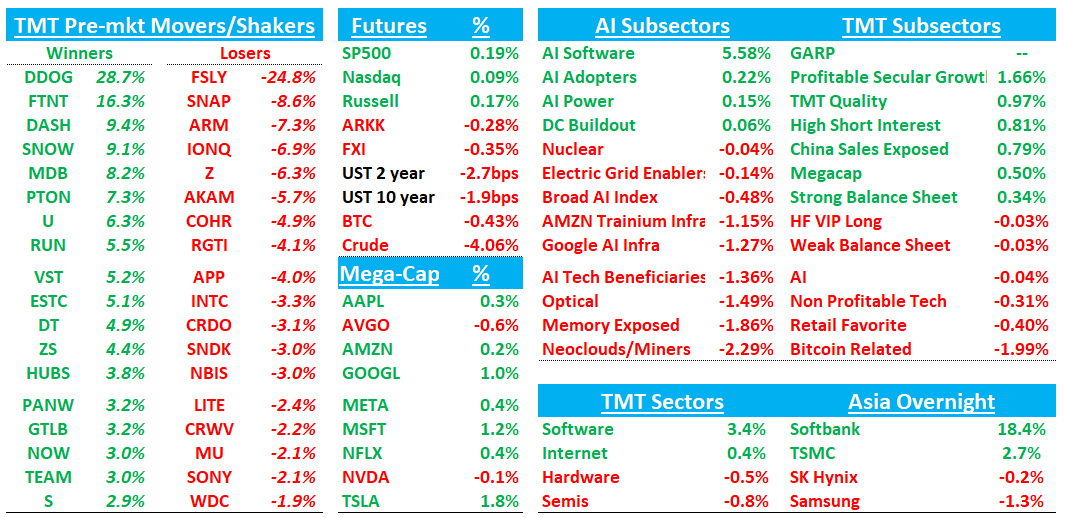

Good morning. Futures flattish. Yields stepping down slightly. Semi names down early following ARM’s miss, and software/internet catching a bid following much better results from DDOG +28% and solid prints from FTNT +16%; DASH +10% and U +6%. Cloud consumption names up early on the back of DDOG with SNOW/MDB +7% — this has been one of the last of AI laggards to regain their mojo and that likely changes after today. Semis -80bps vs software +340bps so big spread early and looks like we could get one of those mean reversion sw/semi days after the massive semi outperformance over the last month+.

We’ll cover earnings from ARM, APP, FTNT, DASH, COHR and DDOG then onto the usual.

Lots to get to, so let’s get straight to.

ARM -7%: Slight beat but missed bogeys; license beat, royalty miss. AGI CPU doubling to >$2B but supply remains gating factor. Language around CPU-to-GPU confused some.

Overall, numbers a bit weaker especially given its multiple and after the huge ramp the stock has had into the print (stock +13% yesterday following AMD), but overall won’t change the mind of the LT CPU bulls on the stock. Disclosed $2B of AGI CPU demand in the letter which had stock up early but then said they don’t have enough supply for the full $2B on the call which caused the sell off. On the call back, mgmt said some customers contacted ARM after Arm Everywhere seeking to place AGI CPU orders to replace x86 CPUs they had planned to procure. Some of those customers reportedly already had memory supply, but ARM did not have additional TSMC 3nm wafer allocation for this calendar year, but could potentially secure more allocation next year.

Language from CPU-to-GPU ratio not changing also cited being ab it confusing, although my takeaways is that there will still be plenty of $ growth for CPUs. Here’s the quote from Rene the call:

The way I think about it is that while the ratios may not go to more CPUs than GPUs from a chip standpoint, they probably will from a core count standpoint. And what do I mean by that? The way to think about Blackwell and Rubin and some of these large accelerators is that they’re pretty much reticle-limited, meaning that the size of the chip is already limited by the amount of area that a mass can print. So it’s not like you’re going to get many, many more GPUs, and then one could argue how efficient those GPUs are as they consume all that silicon. On the flip side, CPUs today, the Arm AGI CPU, for example, it’s 136 CPU cores, Vera, that’s 88. As I mentioned earlier, could I see those core counts doubling or quadrupling over the next number of years? Absolutely. Does that mean that, oh, the ratio of chips stay the same if one chip has 500 cores and it used to have 136 cores. So clearly, the ratios are going to -- are going to change from a CPU core count, maybe not a chip count. Where we’ll see the growth in my opinion is not so much in the head node to a GPU architecture because it’s a little bit fixed given the way the GPU is architected and how it feeds to CPU. But will you see many, many more CPUs inside a data haul, dedicated racks of CPUs that are doing agentic orchestration and scheduling and management, 100%.

The #s:

Revenue was $1.490B, +20% y/y (last q +26% y/y) vs Street ~$1.470B, +~19% y/y; non-GAAP EPS was $0.60 vs Street $0.58 and non-GAAP OM was 49.1% vs Street ~47.5-47.7%. License was the upside driver at $819M, +29% y/y vs Street ~$775M, while royalty was softer at $671M, +11% y/y vs Street ~$700M as mobile weakness and a tough comp masked data center strength.

F1Q27 guide was better on EPS: revenue $1.260B, +20% y/y vs Street ~$1.246B, and non-GAAP EPS $0.40 vs Street ~$0.36-$0.37, helped by lower OpEx.

AGI CPU demand is now >$2B across FY27/FY28 vs prior $1B, but mgmt kept the revenue outlook at $1B due to wafer, memory, packaging and test capacityMgmt said mobile unit growth flipped negative in the latest quarter and the overall market should remain “flattish, maybe slightly negative,” with the lower end most impacted. ARM’s mix is skewing toward premium phones, where Armv9 and CSS lift royalty rates, so mgmt expects cloud AI and autos to more than offset lower-end mobile pressure.

Bull vs Bear Debate

The bull case is that ARM is transitioning from a high-quality semiconductor IP royalty story into a broader AI infrastructure platform with multiple growth vectors: legacy IP/CSS royalties, higher royalty rates from Armv9 and CSS, custom silicon attach at hyperscalers, and now a merchant AGI CPU business. The quarter reinforced the bull case because data center royalties more than doubled y/y, mgmt said they should double again in FY27, and AGI CPU demand doubled to >$2B in only six weeks. Bulls view that as an unusually strong early demand signal, especially because mgmt described customers that already use ARM software and can deploy rack-level solutions with relatively low friction.

Bulls also argue that agentic AI expands the CPU role. The narrative is not just “more GPUs need some CPUs,” but that agentic workloads require orchestration, scheduling, memory management, security and data movement, all of which increase CPU intensity. Mgmt framed the data center CPU TAM at >$100B by 2030 and explicitly suggested that number may be undercalled. If ARM becomes the default CPU architecture for AI accelerators, including NVIDIA Vera/Rubin, AWS Graviton/Trainium, Google Axion/TPU and Microsoft Cobalt/Maia ecosystems, the company can compound well above traditional semiconductor IP growth for several years.

The bear case is that the stock has already priced in most of the AGI CPU upside before the business has proven supply, margins, customer concentration, competitive positioning or scale. Bears point out that mgmt did not raise the $1B FY27/FY28 revenue outlook despite >$2B of demand because supply chain capacity is not yet secured. That means the most exciting datapoint is not yet a revenue forecast. Bears also argue that moving from IP to merchant silicon introduces new risks: lower gross margins, working capital needs, supply allocation risk, customer support obligations, and possible tension with ARM’s existing IP customers.

Bears also focus on the quality of the quarter. The revenue beat was driven by licensing, not royalties, and royalty revenue missed Street despite data center strength because smartphone weakness and a tough comp dragged the line. Related-party revenue remained meaningful, including SoftBank design/licensing revenue, and some reports flagged revenue quality concerns around related-party contribution. FCF was also weak versus Street. In the bear framing, ARM remains exposed to handsets, faces competition from x86, custom ARM CPUs, and RISC-V, and may have an ambitious 15% AGI CPU share target in a market where Meta, OpenAI and other large customers are likely to multi-source. Finally Bears say stock is way too expensive: If FY27 revenue grows around 20% to ~$5.9-$6.1B, but FY28 AGI supply is limited and EPS lands closer to ~$2.7-$2.9 rather than $3.2+, then paying ~80x FY28 EPS is harder to justify.