TMTB Morning Wrap

Good morning. Futures -50bps as investors digest NVDA print (down the fairway print) and news from the Middle East (Reuters reporting Iran’s Supreme Leader has issued directive that the country’s near weapons-grade uranium should stay in Iran/US and reports that Iran has restarted drone production and is rebuilding key military capabilities faster than expected after US-Israeli strikes.)

Yields popping again up 4-6bps across the curve. Oil +2.5%.

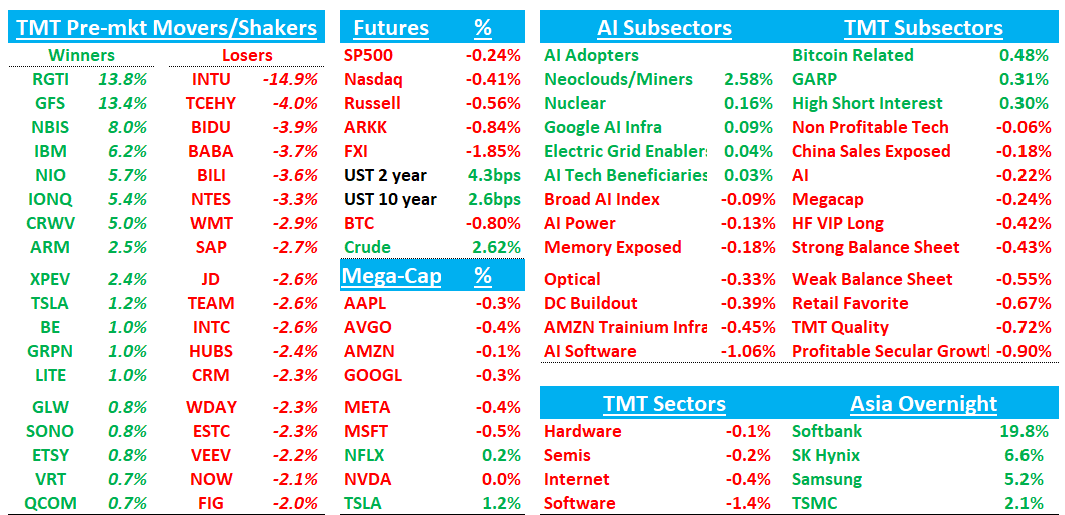

Asia mixed with KOSPI strong: TPX +1.64%, NKY +3.14%, Hang Seng -1.03%, HSCEI -1.51%, SHCOMP -2.04%, Shenzhen -2.4%, Taiwan TAIEX +3.37%, Korea KOSPI +8.42%, Australia ASX 200 +1.47%. Lots of movers overnight in Asia: Samsung +6% / SK Hynix +7%, Kioxia +9%… Softbank +19% on OpenAI IPO news and ARM being up 15% yesterday. LG electronics +30% on positive physical AI mention from NVDA. Substrates up with Ibiden +13%, Kinsus/Unimicron +10%, helped by the NVDA CPU commentary.

Quantum names up on news Trump admin funding some companies. NBIS +8% on news of pricing increase. Software -1.5% lower following the INTU print that is fanning fears of AI disruption with Semis roughly flat.

Today we have the SPOT investor day, and earnings from TTWO, WDAY, and ZM

We’ll hit on NVDA and INTU -14% first then get to the usual, where we have a lot of good stuff to cover today.

Let’s get to it…

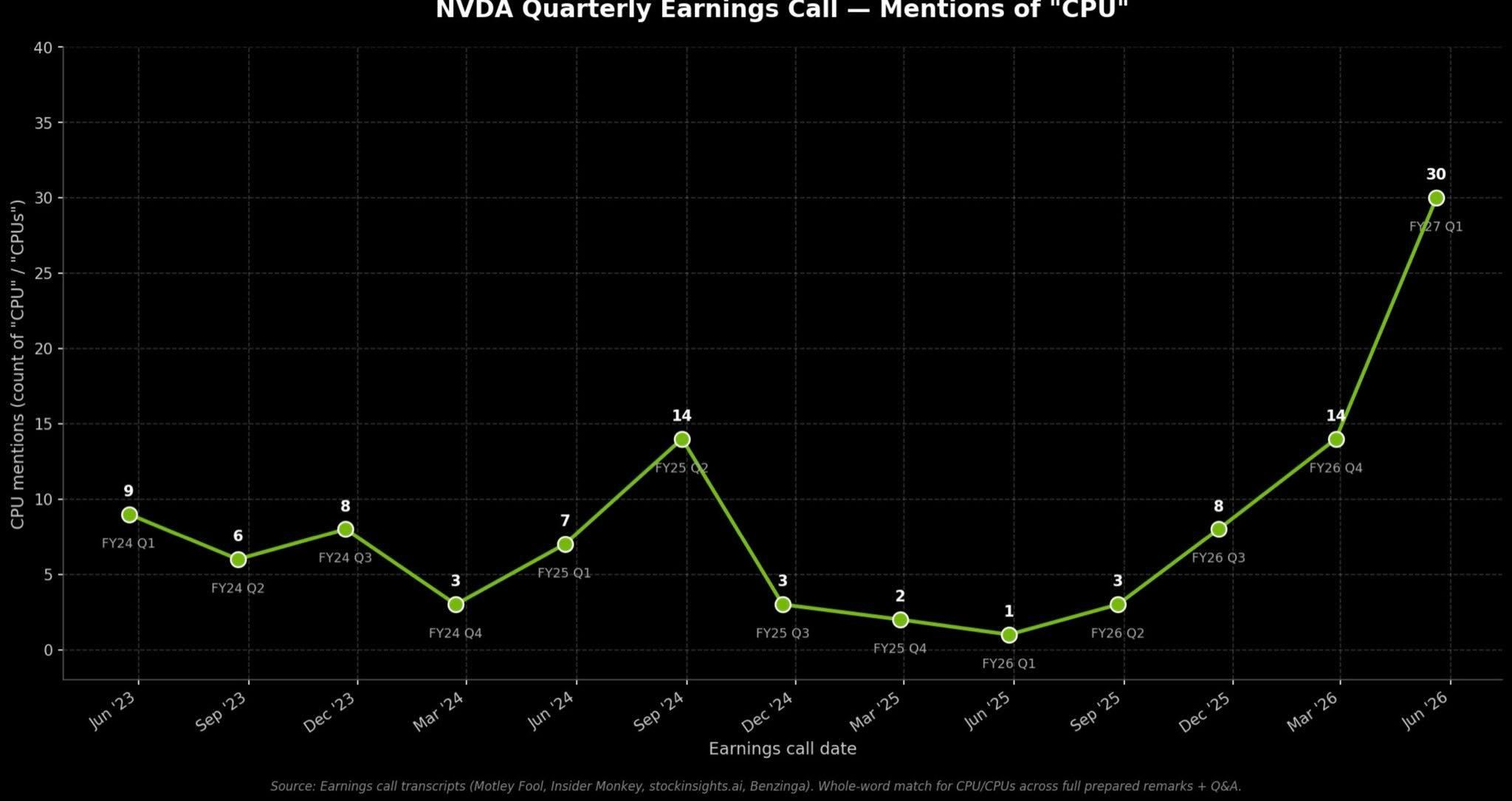

NVDA: Solid #s pretty much in line with buyside bogeys… $80B buyback…CPUs steal the show. Jensen bullish on the call as expected.

Q1 Revs $81.6B vs Street at $79B and Q2 guided to $91B at the mid point vs. street at $87.5B. Both #s pretty much inline with bogeys heading into the print. GMs also roughly inline with street/bogeys. Overall, buyside numbers not really moving up with most still at $10/$15/$18-20 for CY26/CY27/CY28 and not much changes in the bull vs bear debate.

Big investor talk overnight wasn’t GPUs but CPUs as NVDA disclosed they have $20B visibility for the Vera CPU this year (all standalone Vera), and also gave an a $200bn TAM # for the CPU opportunity, which would make them the largest CPU maker in Year 1 of selling CPUs.

In terms of read-throughs, positive for ARM although we don’t know the actual #s from licensing deal with Vera. The $200B TAM is > than the $125B Lisa Su threw out on AMD’s EPS call, but AMD -2% down on concerns of share loss (INTC -3% down on similar fears).

Key Takeaways:

Q1 Data Center revenue was $75.246B, +92% y/y and +21% q/q vs Street $73.504B, with compute up ~18% q/q and ~77% y/y, and networking up ~35% q/q and ~199% y/y. Networking revenue hit $15 billion for the single quarter, with a yoy growth rate nearing 200%. Hyperscale was $37.9B, +115% y/y and +12% q/q, while ACIE was $37.4B, +74% y/y and +31% q/q.

Mgmt said Vera Rubin starts production shipments in Q3 and ramps into Q4, with major customers already lined up.

Jensen pointed out that although SRAM-architecture-based LPs (LPUs) possess advantages in low latency and high interactive token rates, their throughput, model capacity, and context handling capabilities are limited. In the long run, they will remain a niche product for specific premium token services, with their current market share being well below 20%.

Mgmt argued NVDA is gaining share in inference, especially after adding Anthropic and broadening coverage across frontier labs. It also emphasized GB300 performance improvements, lower cost per token, and Rubin’s role as the next inference platform.

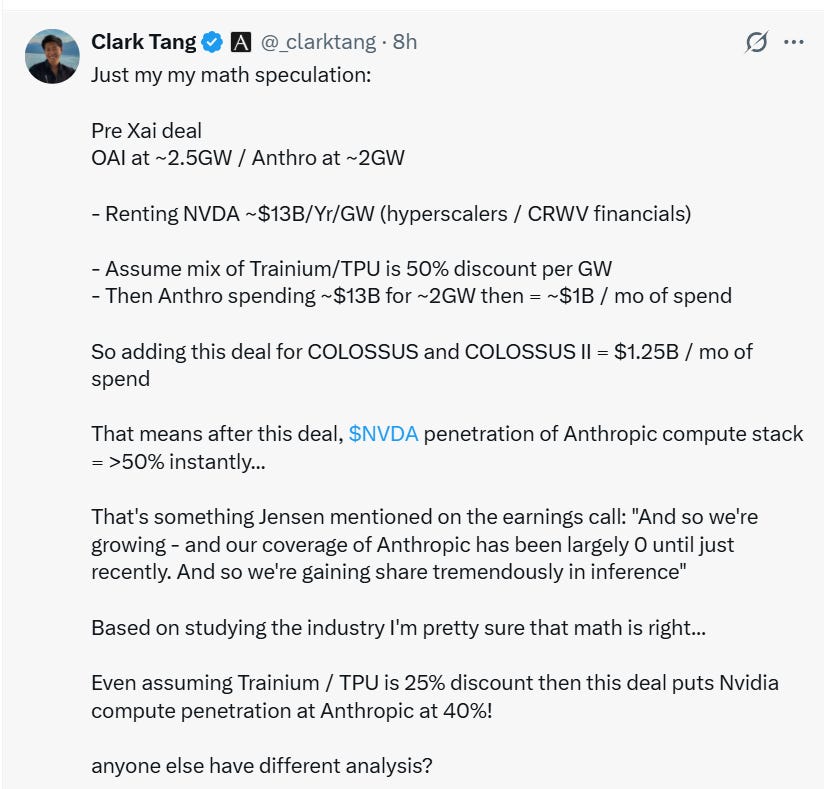

Interesting math on NVDA penetration at Anthropic…