TMTB Morning Wrap

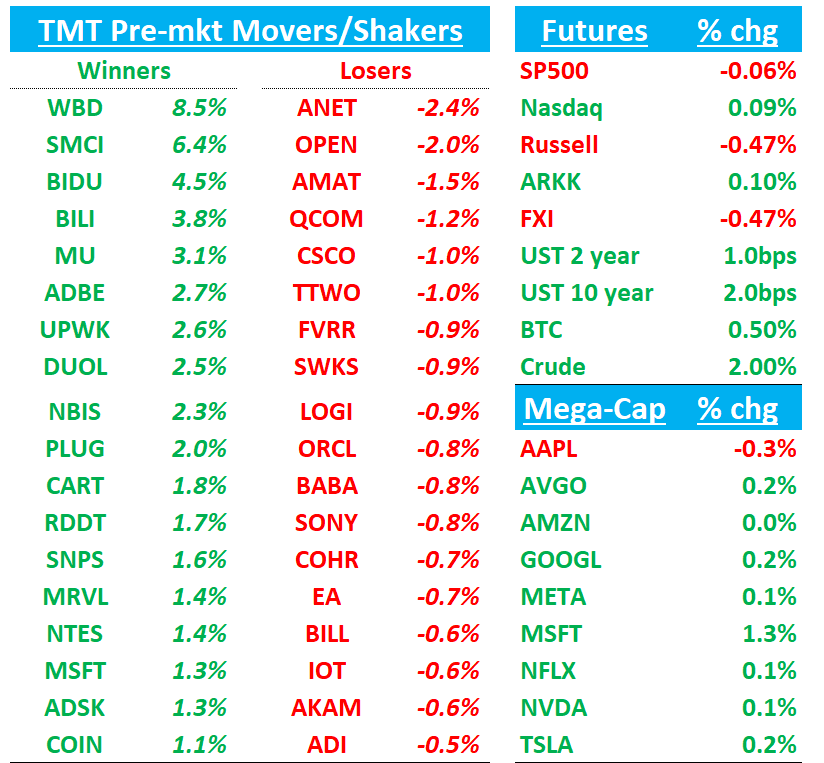

Good morning. Futures slightly up on a day of quiet news flow. Asia finished higher with China +1% and HK Tech +170bps while Europe mixed. BTC +50bps. Yields ticking up slightly. ADBE recap first then Research/News…Let’s get straight to it…

ADBE +3% solid beat/raise as AI KPIs better but print unlikely to change bull vs. bear debate

DM NNARR of $500M slightly above bogeys. Revenue $5.988B, +10% y/y (last q 11% y/y) vs Street $5.918B. DM rev growth 11% cc vs street at 10%. Raising FY DM revs +100M vs beat by +75M. AI KPIs tracked better (AI‑first ARR >$250M; AI‑influenced ARR >$5B), and FQ4 / FY25 guides ticked up FY DM ARR growth raised from 11% to 11.3%

Bull vs Bear Debate

Bulls argue Adobe’s AI flywheel is finally visible in the numbers: AI‑first ARR over $250M only two quarters after the initial disclosure; AI‑influenced ARR >$5B spanning DM and DX; and steady NNARR stabilization despite last year’s pricing actions. They point to AEP & Apps +40%, AEP AI Assistant ~70% adoption, and GenStudio/Firefly Services scaling as proof points that agentic AI (agents + LLM Optimizer) will expand seats, ARPU, and consumption across enterprise and prosumer workflows. Bulls will say 3P models integrated into Adobe apps (Gemini/Veo/Imagen, OpenAI, etc.) reduce model‑disintermediation risk while keeping Adobe “OS‑for‑creativity” control of the workflow. With Q4/FY25 guides up and OM discipline intact (~45.5%/~46%), bulls see a path back to 11–12% ARR growth and teens EPS growth through FY26 as AI attach broadens and Express/Acrobat funnel converts. Bulls will say stock is cheap and buying back 10% of the co…18x FY 27 not unreasonable as Ai visibility + narrative improves, which is a $450+ stock.

Bears will continue to point to LLM/AI/Canva/META structural/competitive threats saying GenAI threatens Adobe’s moat as content tools embed inside ad platforms and LLM providers, potentially compressing ARPU and shifting work to consumption from seats; bears also worry that SMBs can stay within Google/Meta ad creation flows. (Mgmt counters that enterprises need multi‑channel orchestration and Adobe integration across channels.) Bears will remain focused on growth deceleration (company‑wide cc growth 11%→10% in Q3; Q4 guide ~9%) and argue the quarter leaned on pricing/mix (Creative Cloud Pro) rather than a clean, organic inflection, with DX guide modestly below Street. They worry about competitive pressure (low‑end content tools, model commoditization) and AI cannibalization risks (fewer pro seats needed as gen‑AI boosts productivity), plus the lack of a clear, quantified AI uplift to DM NNARR beyond the $250M baseline. On valuation, bears will say stock shouldn’t trade above 15x given the secular/structural risks and has potential for downside as LLM competition like Nanobanana eats into the CC installed base.

No strong view here…

Key takeaways:

NNARR stabilization. DM NNARR ≈$500M, roughly flat y/y after two soft quarters (‑6% y/y in Q2), aided by Creative Cloud Pro pricing and AI attach (esp. Acrobat AI Assistant).

Q4 revenue $6.075–$6.125B (above cons. $6.085B); non‑GAAP EPS $5.35–$5.40 (above $5.34). FY25 revenue/DM ARR growth/EPS raised; OM reiterated ~46%

Mgmt is assuming consistent macro and retention; swing factors are sustained CC Pro momentum and AI‑first products/Acrobat; expect normal Black Friday seasonality and an enterprise bump vs. Q3.

AEP & Apps subscription +40% y/y, AEP AI Assistant adoption ~70% of eligible customers; launched AEP Agent Orchestrator and LLM Optimizer (EA) to help brands show up in LLM results—supporting the agentic AI narrative.

Acrobat + Express MAUs +~25% y/y; Acrobat AI Assistant units +40% q/q; >14k orgs added Express in Q3 (4x y/y). These usage signals bolster the freemium to paid conversion story

“Consistent macro, stable retention” assumptions for Q4.

Mgmt reiterated model choice (Firefly + 3P models) inside Creative Cloud/Express and cross‑cloud (One Adobe) deals +60% y/y, arguing Adobe is the mission‑critical creative AI partner

New subscribers remain the primary growth lever, followed by cross‑sell/upsell, then pricing; the second phase of CC Pro price increase (Aug) was already embedded in prior guidance.

3P model usage accelerating (e.g., Gemini Flash 2.5); customers get credit entitlements and pay rate‑card premiums when exceeding allotments; North Star is 100% of revenue AI‑influenced over time.

Mgmt said to expect mid‑40s OM through the investment cycle, offset by cloud efficiencies and productivity