TMTB Morning Wrap

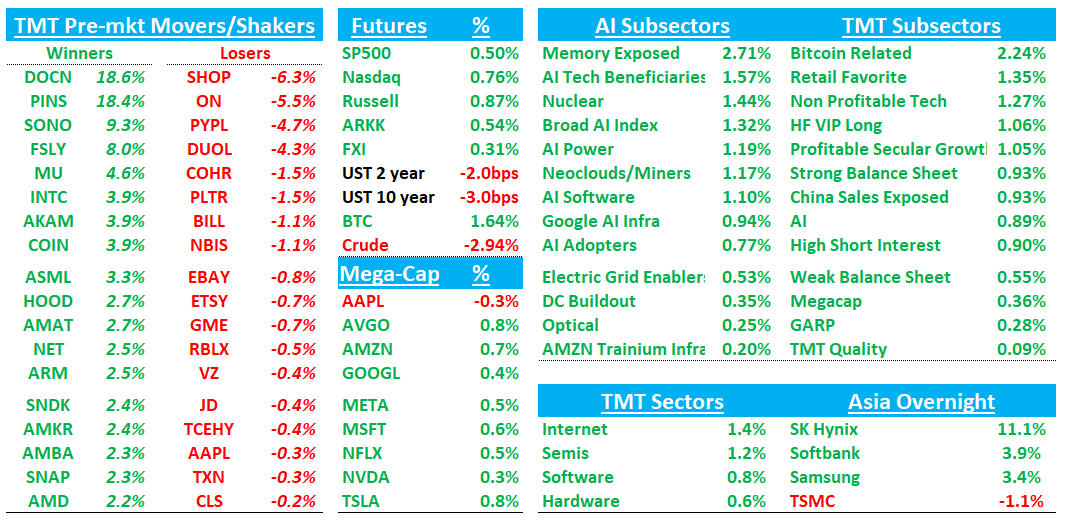

Good morning. Futures +75bps with strength across the board and Oil -3% as ceasefire between US/Iran seems to be holding for now with no further escalation following yesterday. Japan, China and Korea were closed yesterday. In the U.S. memory names leading the way higher again with MU +4.5%, SNDK +2.5% while INTC +4% on reports that AAPL exploring using them and Samsung as a foundry partner.

We’ll hit earnings first - PLTR, PINS, ON, DUOL - then dive into the usual.

Let’s get to it…

PLTR -1%: another blowout beat-and-raise and accel: 1Q revenue +85% y/y (last q +70% y/y) vs Street +~74%, with FY26 revenue guide raised to +71% y/y vs Street +~61-62%. Main nit that commercial growth decel’d and missed street by $10M

The #s:

US revenue $1.282B, +104% y/y, with US Gov $687M, +84% y/y, and US Commercial $595M, +133% y/y headline, +143% adjusted for a customer transition to US Gov.

non-GAAP OM 60.2% vs Street ~56.8%, EPS $0.33 vs Street $0.28, adjusted FCF $925M, 57% margin vs Street ~$833M.

The main negative optic was US Commercial missing Street by ~$10M and decelerating vs +137% y/y last q, but mgmt attributed this to a ~$25M reclassification and raised US Commercial FY26 guide to >120% growth.

Key Takeaways:

1Q revenue beat Street by roughly $90-$95M, but FY26 revenue guide was raised by ~$466M at the midpoint to $7.656B, implying mgmt is not treating the quarter as a one-off

US Gov grew +84% y/y to $687M vs Street ~$606M, and mgmt pointed to Maven usage doubling over the last four months and 4x over 12 months, plus ShipOS, USDA, and defense industrial base demand. The customer transition from US Commercial to US Gov also highlights a potential flywheel where commercial pilots can scale under gov funding.

Headline US Commercial grew +133% y/y to $595M vs Street ~$605M and last q +137% y/y, which explains the after-hours debate. However, adjusted for the customer moving to US Gov, growth would have been +143% y/y and +22% q/q, and FY26 US Commercial guide was raised to >$3.224B, >120% y/y.

Mgmt framed lower model costs as a tailwind, not a risk, because cheaper inference expands use-case demand while increasing need for governed, auditable AI infrastructure

Mgmt said customers are replacing legacy software and highlighted PLTR replacing its own CRM with an AIP-built AI-first solution.

Mgmt described US demand as overwhelming and supply-constrained, while Europe/international remains comparatively muted.

The callback clarified that the US Commercial-to-US Gov recategorization came from a private commercial entity funding a reindustrialization program that worked well enough for the gov to take over and scale. Mgmt still felt good enough on US Commercial to raise the guide, with Q2 implied US Commercial sequential growth of ~20-21% and a ramp into year-end.

On competition, mgmt said PLTR does not typically run into Anthropic in the field and sees more synergy with AI labs, while customers are raising the bar for production-grade software and economic value.

Bull vs. Bear Debate

The bull case is that PLTR is becoming the operating system for production AI, especially in environments where failure is unacceptable: defense, manufacturing, financial services, insurance, healthcare, and regulated enterprise workflows. Bulls see the quarter as a clear proof point that AIP is not just a demo-layer or chatbot wrapper. Revenue growth accelerated to +85% y/y, US revenue crossed +100% growth, US Commercial still grew +133% headline and +143% adjusted, and US Gov accelerated to +84% y/y. The strongest part of the bull case is that the largest FY26 guide raise came despite already aggressive expectations, suggesting mgmt sees conversion of AIP pilots and existing deployments into larger, recurring programs.

Bulls also argue PLTR is structurally advantaged versus both legacy SaaS and model labs. Legacy SaaS is vulnerable because PLTR can replace workflows rather than sit on top of them, while model labs are complementary because PLTR is model-agnostic and provides governance, ontology, security, auditability, and operational execution. The call and reports emphasized that cheaper inference increases token usage and AI workflows, creating demand for a system that can govern actions and cost. The result is a company growing faster than almost any public software company at scale while producing 60% non-GAAP OM and nearly 57% adjusted FCF margin.

The bear case is not that the quarter was weak. It is that the stock already prices in extraordinary durability, and even modest deceleration could compress the multiple. Bears point to headline US Commercial growth slowing to +133% y/y from +137% y/y last q and missing Street by about $10M. They acknowledge the customer transition explanation, but argue that the cleanest public segment optic still matters because US Commercial is the highest-profile part of the story. They also point to RPO growth decelerating to +134% y/y from +143% y/y, TCV growth decelerating to +61% y/y after an unusually strong 4Q, and international remaining meaningfully weaker than US.

Bears also see operational and competitive risks. If PLTR truly has overwhelming demand and only a small sales footprint, then the company may be underinvesting in GTM and leaving TAM uncaptured. If PLTR ramps expenses, margins could moderate; if it does not ramp, bears argue growth may eventually bottleneck. They also worry about gov concentration, budget timing, CR risk, political scrutiny, Europe/international pushback, high pricing, and potential competition from AI labs, hyperscalers, data platforms, and vertical AI applications. The risk is that the company remains exceptional, but the stock’s valuation requires “more than exceptional.”

PINS +17%: Clean beat and raise (1Q revs 18% vs. 13%), with the narrative improving on UCAN acceleration, large-retailer stabilization, and AI-driven ad product traction, partly offset by unchanged FY margin guidance and international/GTM execution risk.

Expectations were very low here and sentiment leaned short this this print will be more than enough but still a long way to regain LO's trust. The core positive was UCAN reacceleration, improving ad pricing, and evidence that AI bidding/measurement is offsetting large-retailer weakness late in the quarter while main pushback overnight centered around EBITDA only reiterated at 29% despite the beat, the GTM changes causing disruption and int’l expected to moderate in Q2

The #s:

1Q Revenue was $1.008B, +17.8% y/y (last q +14.3% y/y) vs Street $964M, +~13%; Adj. EBITDA was $207M, 20.5% margin vs Street $177M, ~18% margin; non-GAAP EPS was $0.27 vs Street $0.25.

FQ2 revenue guide was $1.133-$1.153B, +14-16% y/y, or +13-15% ex-FX, vs Street ~$1.115-$1.120B, +~12%; Adj. EBITDA guide was $256-$276M vs Street ~$260-$265M. On the callback, mgmt said FQ2 guide appears to embed a full quarter of better exit trends from large advertisers, so further upside likely depends on continued measurement adoption and less GTM disruption.

Key Takeaways:

UCAN revenue was $750M, +13% y/y vs Street $715M, improving from +9% last quarter and carrying much higher ARPU than international

Ad impressions grew +24% y/y while ad pricing declined -5% y/y, a sharp improvement from -19% last quarter. The better pricing mix was driven by stronger UCAN demand and lower growth in international impressions, which had previously pressured pricing.

Mgmt said large retailers remained a headwind, but the headwind was partially offset late in the quarter by AI-driven bidding and ad platform improvements. Macro was described as broadly consistent, with large retailers still navigating tariff-related margin pressure.

Mgmt repeatedly highlighted that revenue growth excluding the largest retailers accelerated relative to FQ4.

. About 30% of lower-funnel revenue is now running through Performance+ campaigns, and adopters grew lower-funnel spend at nearly 2x the rate of non-adopters. This supports the bull case that PINS is moving from an upper-funnel inspiration platform toward a more credible performance ad platform.

AI: PinRec improved search fulfillment by ~180 bps and reduced CPA/CPC by ~180 bps; search ranking context windows expanded 30x and improved saves by ~390 bps; ROAS model improvements drove gains of up to 11% in experimentation; one large advertiser saw 15-20% LTV ROAS improvement from measurement integration.

Mgmt is changing sales coverage, incentives, technical sales accountability, and international leadership

On the callback, there was also discussion that COGS deleverage should diminish in 2H after the AWS renewal, helping offset tvScientific drag. Customized measurement work is expected to pilot with more advertisers over the next few quarters and broaden toward smaller advertisers later in the year.