TMTB Morning Wrap

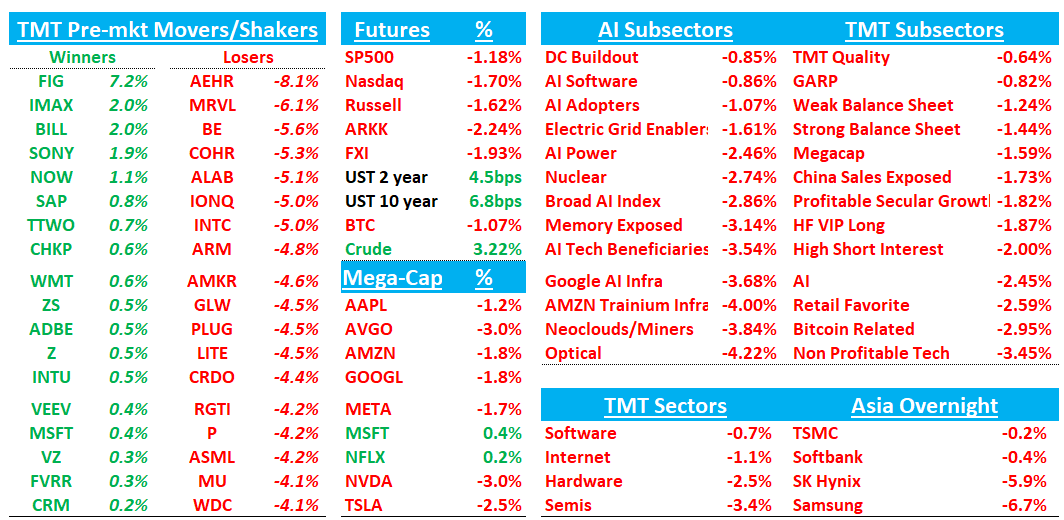

Good morning. Futures -1.7% to start the day. Lots of questions on the weakness. Hearing several things: 10 year just crossed 4.5%, possible strike at Samsung, Kioxia/AMAT down after solid beats, general profit taking after record rally with semis still very extended, and a bit of sell the news on Xi-Trump which failed to yield any significant announcements while no deal on Iran continues to be the norm.

Asia was generally red: TPX -0.39%, NKY -1.99%, Hang Seng -1.62%, HSCEI -1.89%, SHCOMP -1.02%, Shenzhen -0.88%, Taiwan TAIEX -1.39%, Korea KOSPI -6.12%. Samsung -6%. Kioxia -9% after a set of good results. SK Hynix -6%

Semis -3.5% early vs software -0.7%

We’ll hit AMAT and FIG first, then onto the usual…

AMAT -2%: Clean beat-and-raise with CY26 Semi Systems growth moving to >30% from >20%, with leading-edge F/L, DRAM and advanced packaging expected to drive >80% of WFE growth in CY26 and a similar mix in CY27.

Overall, very solid print andhigher than buyside expects, especially the $8.95B midpoint rev guide vs expects of $8.6B+. Some profit taking going on this morning with semis down.

Revenue was $7.910B, +11.4% y/y (last q -2.1% y/y) vs Street $7.674B, +~8.1% y/y; non-GAAP EPS was $2.86 vs Street $2.68; non-GAAP GM was 50.0% vs Street 49.3%.

FQ3 guide was materially above: Revenue $8.950B, +22.6% y/y vs Street $8.153B and bogeys of $8.6B+, +~11.7% y/y; non-GAAP EPS $3.36 vs Street $2.88; non-GAAP GM 50.1% vs Street 49.4%.

Key quote:

“I'm having constant conversations with customers and they're looking at '27 and they're looking at '28. But again, because the compute demand is growing so quickly … we're modeling incremental CPU demand, incremental DRAM and NAND demand. That's a meaningful increase on top of what we had been forecasting previously.”

Key Takeaways:

Mgmt said demand strengthened across nearly every leading indicator, CSP capex is rising, most leading-edge logic and DRAM fabs are full, customers are freeing up cleanroom capacity, and large customers are giving rolling eight-quarter forecasts.

Mgmt highlighted token growth, agentic AI and future physical AI as incremental layers of compute demand. Agentic AI was described as more CPU-intensive and also supportive of DRAM/NAND, which matters because it broadens AMAT’s exposure from leading-edge foundry into memory and packaging.

Leading-edge F/L, DRAM and advanced packaging are where AMAT has strong share and where mgmt expects >80% of incremental WFE growth in 2026 and a similar profile in 2027. FQ2 Foundry/Logic was the standout at $3.997B, +12% y/y vs Street $3.669B, while DRAM was below Street in the quarter but still grew +19% y/y, and FQ3 guidance points to accelerating Semi Systems.

Non-GAAP GM hit 50.0%, with Semi Systems GM around 54.8% in FQ2. Mgmt attributed the improvement to richer portfolio mix, value-based pricing and manufacturing cost work, while saying new tools and solutions should support continued, though gradual, GM improvement.

Mgmt expects packaging revenue to grow >50% in CY26, highlighted leadership in HBM and 3D chiplet stacking, and tied the NEXX acquisition to larger body packages for AI accelerators.

AGS revenue was $1.665B, +17% y/y vs Street $1.609B; mgmt raised the medium-term growth framework to mid-teens, with this year potentially higher due to utilization and new fab ramps. The service story is helped by the expanding installed base, higher fab utilization, AIx software, remote monitoring and output/yield optimization.China was 26% of total revenue, or about 24% of Semi Systems plus AGS, down from last quarter; mgmt said China and global ICAPS should be flat to slightly higher in CY26. On export restrictions / Huawei, mgmt did not comment in detail but said restrictions were already reflected in the quarter guide and CY outlook. I did not see explicit tariff commentary in the uploads.

Bull vs. Bear Debate:

The bull case is that AMAT is sitting at the center of the highest-value parts of the AI compute capex cycle. The company is not just benefiting from general WFE growth, but from the specific parts of WFE that are growing fastest: leading-edge foundry/logic, DRAM/HBM and advanced packaging. This quarter supported that view as FQ3 guidance was materially above Street, CY26 Semi Systems growth was raised to >30%, advanced packaging is expected to grow >50%, and mgmt said large customers are providing eight-quarter forecasts. The bull read is that AMAT’s product breadth, deposition strength, conductor etch share, eBeam/process control, GAA exposure and packaging portfolio give it multiple ways to monetize AI-related transistor, memory and packaging complexity.

Bulls also argue the cycle is becoming more durable because demand is broadening beyond training GPUs. Agentic AI adds CPU, DRAM and NAND demand, physical AI could become another layer later, and customers are now trying to pull in equipment by freeing up cleanroom capacity. This quarter, mgmt pushed back implicitly on the idea that 2026 is just a pull-forward: 2027 still looks strong and customer forecasts extend into 2028. AMAT also has operating leverage: GM crossed 50%, Semi Systems GM is approaching 55%, and opex is expected to grow slower than revenue, creating a path toward mid-30s operating margins over time.

The bear case is that expectations have moved very quickly, valuation is no longer cheap on an absolute basis, and WFE remains a cyclical equipment market even when AI is the current driver. Bears will point out that cleanroom availability and supply chain readiness are constraints, which means revenue upside may not be linear if customer timing slips. They will also argue that some of the strongest upside has already been reflected in the stock, which was up sharply into the print, and that a beat-and-raise may not be enough if investors were already underwriting a multi-year AI capex supercycle. The fact that DRAM and NAND were below Street, even though the overall print was strong, gives bears some room to argue that the quarter was F/L-heavy and that memory timing remains uneven.

Bears also focus on AMAT’s broad portfolio and risk pockets. ICAPS and China are not collapsing, but they are not driving the same upside as AI-related leading-edge WFE, and legacy-node exposure faces China competition and export restriction risk. NAND remains a smaller portion of Systems revenue and AMAT participates less in NAND upgrades, which could matter if NAND becomes a bigger part of future WFE.

FIG +7%: Solid beat/raise with AI adoption a standout

Numbers very good should be good enough for a highly shorted stock with AI disruption risk as print helps address some of the core bear fears to a certain extent, but remains to be seen how much follow through we see as tough for the print to truly dispel LT competitive/AI fears.

Key stat: >75% of over-limit org/enterprise users continuing to consume credits and >95% remaining active.

The #s:

Revenue was $333.4M, +46.1% y/y, accelerating from +40.0% last q, vs Street $316.0M, +38.5%; non-GAAP EPS was $0.10 vs Street $0.06; non-GAAP OM was 15.6% vs Street 8.9%.

Q2 revenue guide of $348-$350M implies +39.8% y/y vs Street roughly $327-$330M, +~32%, and FY26 revenue guide moved to $1.422-$1.428B, +35.0% y/y vs Street ~$1.371B, +~30%.

Key Takeaways:

Credit limits were enforced March 18, so Q1 only had a partial-quarter benefit, but early customer behavior was strong: >75% of org/enterprise users who were previously over credit limits continued consuming credits in April, >95% remained active, and Pro teams buying AI add-ons had >3x the average annualized spend of those that did not. This is the cleanest evidence that AI can be a monetization tailwind rather than simply a cost headwind

NDR for >$10K ARR customers rose to 139%, up 3 points q/q and the highest level in more than two years, while $10K+ ARR customers grew +37% y/y and $100K+ ARR customers grew +48% y/y. FIG also ended with ~690K paid customers, +54% y/y, and mgmt said >60% of paid customers above $10K ARR added full seats at renewal.

Roughly 60% of $100K+ ARR customers used Make weekly, up from >50% last q, and MCP weekly active users in Design grew 5x q/q. Among $100K+ ARR customers, those using MCP grew full seats ~70% faster than those not using MCP, suggesting AI agents and code-to-canvas workflows are pulling users into FIG rather than bypassing it.

Gross margin fell to 82.3% vs Street 83.4% and down from 86.2% last q as AI usage expanded. However, non-GAAP operating income of $52.1M and OM of 15.6% were far above Street $28-$29M and ~9%, while FCF of $88.6M and 26.6% margin crushed Street $22.7M and 7.2%.

gmt called out stronger-than-expected seat expansion across entire organizations, growth in new customer acquisition and expansion, international revenue +48% y/y, and one hyperscaler agreement with >35,000 paid seats.

Mgmt specifically addressed Google and Anthropic-related concerns, saying Google remains a partner and that a Google product was not “getting in the way” in a substantial way, while Anthropic “can’t” be dismissed. The stated differentiation was FIG’s performant multiplayer canvas, deep product context, and ability to unify AI, design, code, and direct manipulation in one platform.

Mgmt said they include what they have “a high degree of confidence in” and wait for sustained data before fully embedding less visible benefits, which matters because Q2 is the first full quarter of AI credit monetization and MCP remains free in beta with potential usage-based monetization later.

Bull vs Bear Debate

Bulls will argue this q materially improves the “AI is a threat” debate because the numbers showed AI helping FIG across multiple levers at once: new paid conversion, seat expansion, credit consumption, and enterprise standardization. The most important point is that Make and MCP are not just features that create engagement, but appear to be pulling users into higher-value paid seats. That matters because one of the biggest bear arguments has been that AI-native tools would compress design and developer seats, but this q showed the opposite: >60% of paid customers above $10K ARR added full seats at renewal, Make weekly usage rose in large accounts, and MCP users grew full seats ~70% faster than non-MCP users.

The other bull point is that FIG now has more than one AI monetization surface. Make is the flagship, but MCP, Weave, advanced image editing, and the AI assistant create a broader credit-consumption layer across the platform. Q1 only captured partial credit-limit enforcement, and Q2 is the first full q of direct AI monetization. Bulls will say the FY26 guide raise is therefore not the end state, especially given mgmt’s stated guide philosophy of only embedding what they have high confidence in and waiting for sustained trends before fully reflecting newer benefits

Bears will argue the q was strong, but it did not fully resolve the two hardest debates: competitive durability and gross-margin structure. The competitive environment is changing quickly, with LLM labs, hyperscalers, AI-native prompt-to-code vendors, and design-adjacent products moving into FIG’s workflow. Mgmt’s commentary was credible, especially around Google and the platform’s multiplayer canvas, but it also acknowledged Anthropic cannot be dismissed. Bears will say it is still early, and that Q1 demand strength does not prove FIG can sustain its moat if AI-native tools increasingly generate usable UI/UX, code, and prototypes outside FIG’s workflow.

The margin issue is the other bear anchor. Gross margin compressed to 82.3%, below Street and down sharply y/y, and mgmt did not give a hard floor. Mgmt is explicitly optimizing for gross profit dollars and adoption rather than a specific gross margin percentage. Bulls may like that strategic posture, but bears can argue that the investment case becomes harder if AI consumption requires structurally lower gross margins, more R&D spend, and continued reinvestment before the revenue model is proven at scale.

Kioxia: Solid beat with better ASPs. Revs at $Y1trn vs. $Y920bn. Op Inc $Y597bn v $Y519bn driven by upside to ASPs, which doubled q/q. Preparing to list an ADR

Stock initially popped but finished down 10%

TECH RESEARCH/NEWS

ANET: Raymond James Upgrades to Outperform on Expanding AI Networking Opportunity

Raymond James upgrades ANET to Outperform, arguing Arista is increasingly differentiated as AI workloads evolve toward larger, more distributed inference/reasoning clusters that require more intelligent east-west networking. The firm highlights growing exposure to AI applications (~40% of sales), expanding opportunities in scale-across networking/WAN extension, and rising adoption tied to AMD accelerator share gains. Raymond James also sees upside from emerging scale-up Ethernet opportunities and believes supply constraints in 2026 could ultimately translate into stronger growth in 2027 as backlog converts.