TMTB EOD Wrap

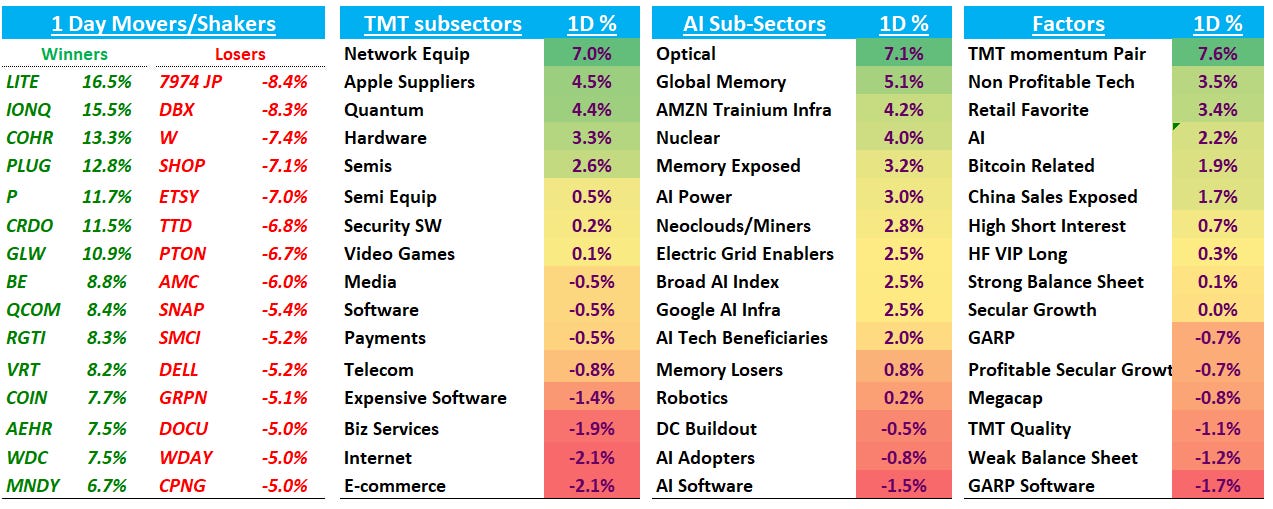

Good afternoon. QQQs +30bps with strength driven by AI semis with strength across the board: optical led the way higher, but memory/HDDs and even NVDA outperformed as the SOX finished +2.7% now up a stunning 65% since the beginning of April.

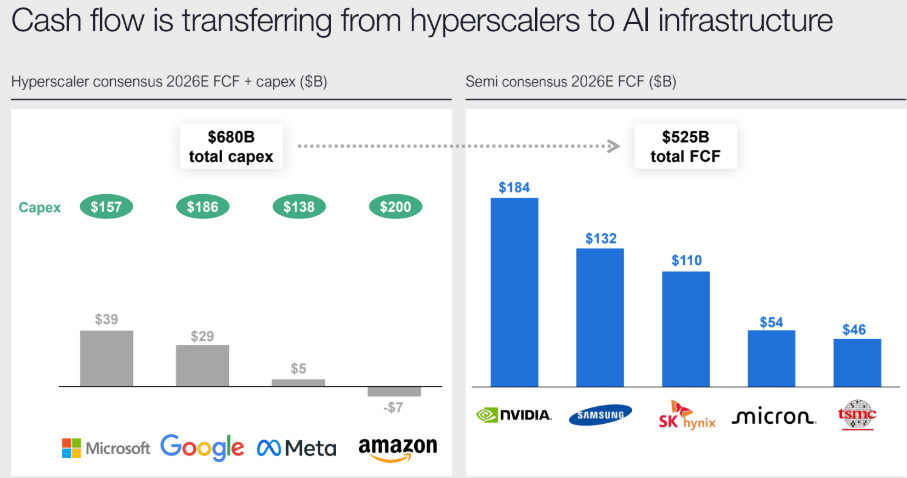

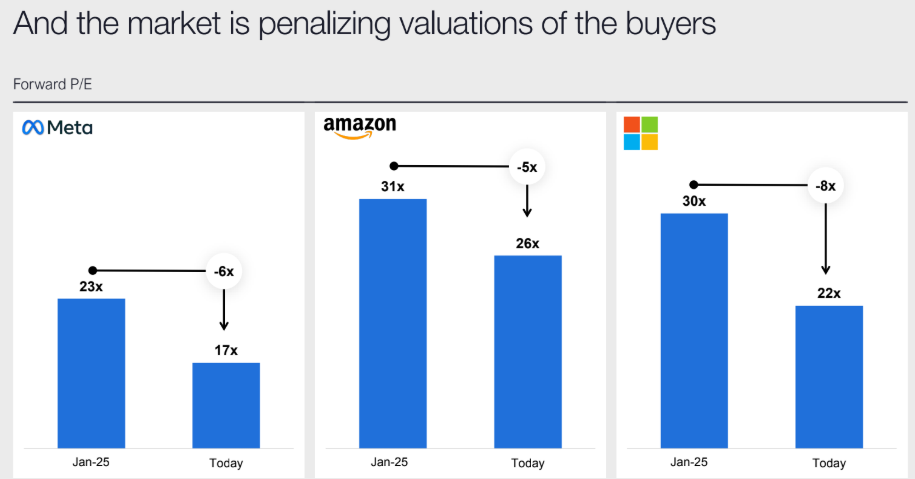

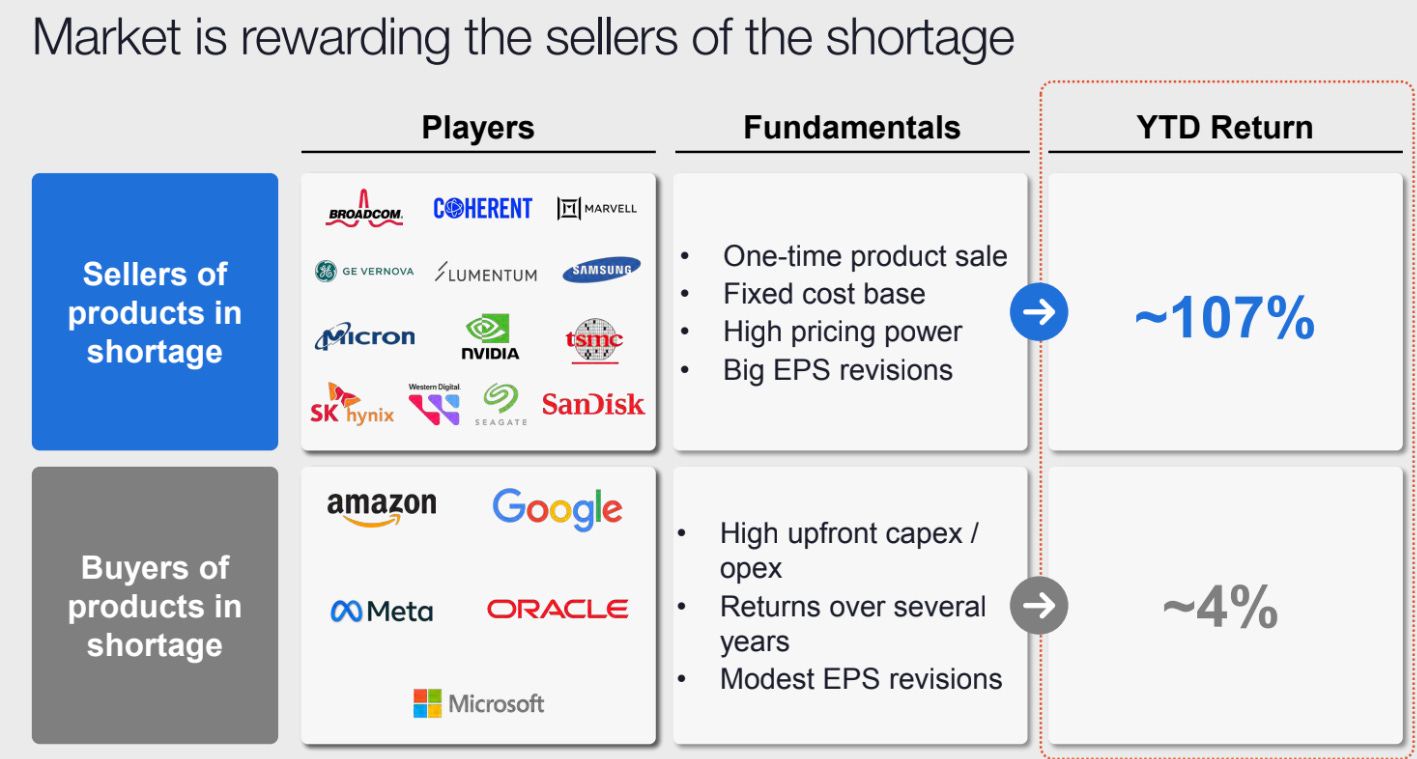

The rotation from software/internet into semis continues. We know app sw is a wasteland, but many charts in internet also making 6 month lows and — outside of GOOGL/AMZN (and ROKU) — decent prints getting sold (RDDT, PINS, DASH, ABNB) and bad prints getting negative follow through (SHOP, NFLX, EXPE, BKNG). Just no appetite right now for anything outside hyperscalers, and even they were weak today, we think in part to a couple Coatue slides being passed around from their slide deck over the weekend:

From a factor perspective, GS pointed out that their High Beta Momentum Pair had their biggest 1d move higher in 5+ years today at 800bps+. Non profitible tech and retail names were also bid while Software/Megacap underperformed

We sent out notes from the Cerebras IPO roadshow here

Let’s get to the good stuff…

AI/SEMIS

A couple other slides from Coatue:

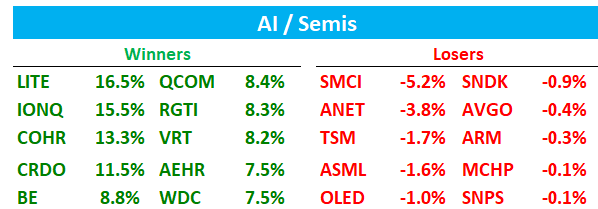

Optical regaining mojo today. LITE +16.5% on the back of the Nasdaq 100 add in addition to some positive news from the Innolight presentation overnight,. Funda.AI had a good recap of the strength today on X:

In China, Innolight’s investor communication today flagged 2.4T and coherent-lite, and that signal is worth paying attention to. The market is no longer just trading the 1.6T ramp — it is already looking ahead to the next-gen architecture. 2.4T / coherent-lite is not a simple bandwidth upgrade: it implies higher lane rates, more complex modulation schemes, longer-reach links, and substantially higher photonic-electronic integration requirements. The higher the technology bar, the better positioned the names with real depth in EML, InP, laser, and OCS/CPO — namely LITE and COHR.

COHR +13%

NOK +8% / CSCO +2% both to new highs….GLW +11% also getting the optical / BofA1 List bid

QCOM +8.5% continues to squeeze into their analyst day. From GFHK: “We believe QCOM is actively developing its data center CPU slated for shipment in 2028, alongside Scale up switch & connectivity silicon for integrated rack-level solutions; we expect further clarity during the upcoming Investor Day on June 24. In a bull case scenario, assuming Qualcomm captures 30% of ARM-based CPU market in 2028 (~4m units, with ASP of $3k and 30% net margin), the resulting $3.6bn in net profit would represent a ~30% boost to its annual non-GAAP earnings. Moreover, Qualcomm is on track to ship its custom AI200 xPU in 4Q26, and we expect the release of subsequent AI250 and AI300 in 2027 and 2028, respectively.”

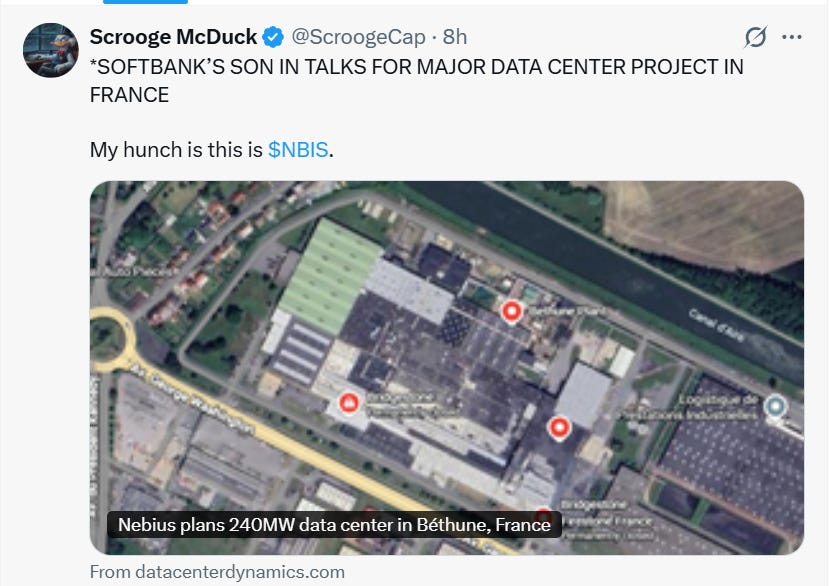

NBIS +5% getting added to BofA1 List and speculation that Softbank’s France DC investment

BofA had a postiive preview of the q saying NBIS currently operates ~220MW of connected power and targets ~900MW by year-end, supporting a sharp revenue ramp into 2H26 as new sites activate and expects margins to improve steadily through the year as utilization and revenue scale increase.

MU +6.5% playing catch up vs. SNDK -1%

INTC +3.5%

HDDs strong: STX/WDC +7% to new highs

NVDA +2% finally breaking out to new highs ahead of Jensen’s DELL keynote (May 18th) and earnings next week

ANET -4% now down 8% following the negative T+1 price action after last week’s print — one of the names with weaker price action in semis right now. Recall, co missed buyside estimates for FY26 (27.7% vs 30%+) and mgmt called out supplier decommits and ~52-week lead time, which some took to mean less 2H’26 and possibly CY27 upside, especially around high-end switch silicon.

ARM -30bps as investors less excited vs INTC/AMD given supply constraints — recall, last week mgmt talked about not having additional TSMC 3nm wafer allocation for this calendar year and said CY27 capacity was not locked in yet, which made investors less excited about their >$2B AGI CPU #.

DELL -6% the big loser in the space today after UBS downgraded saying much of the upside priced now and expects future revisions to be more modest.

BE +8% more digestion from the brookfield earnings call on Friday. Barclays was also out raising #s and PT to $250+

TXN +3.5% as chatter on X pointed to another price increase -link

Other analogs strong as well: NXPI +4%; ADI +1.5%

TSM -2%: guessing investors not liking all the positive INTC/Samsung foundry news as of late

INTERNET

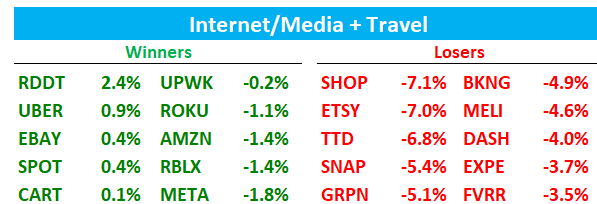

Large cap weakness: AMZN -1.3% / META -1.8% / GOOGL -3%. Didn’t see much news here but think GOOGL likely following through on some of the weaker Yipit data that came out on Friday pointing to a 1-2ppts search miss so far in Q2. Other 3p providers still showing a 1-2 ppts beat so will be interesting to see which way these converge as the q goes on.

ETSY -7% / EBAY +40bps as MS was out with their recent consumer survey pointing to sharply diverging trends between both. ETSY’s purchase intent fell 20ppts since February to the weakest level among surveyed retailers — MS says this raises concerns that the recent GMS accel was driven by tactical factors vs. structural improvements. Some fast-money types were hiding out in this long vs other internet names as 3p data has generally held up pretty well (3p was showing a HSD beat to Q2 so far), so this bit of news pulled the rug out from the trade.

NFLX -2.3% almost back to the gap fill from the WBD deal breaking. Upfronts this week (unclear if we’ll get anything incremental to ads). Risk/Reward definitely more interesting here with $80, or $5 down = 20x CY27 EPS. But man does narrative not sound interesting with engagement concerns, no exciting catalysts on the horizon (in fact, World cup likely a pot’l negative for engagement in q3), and 3p data calling out increased churn following their price increase. Not to mention, everything in internet trades like a wasteland. Still — it’s a decent spot on the chart as can use that gap fill (about 1% lower) as a stop on a very liquid stock. Maybe due for some mean revesion.

SHOP -7% following through to the downside after last week’s weaker print and now breaking to 10 month lows. Investors not liking the decel to high 20s after several quarters at 30%+ as AI debate continues on the stock: “The broader bear debate is whether AI changes the value chain in a way that reduces SHOP’s economic leverage over time. Mgmt argued forcefully that agents connect into SHOP rather than bypass it, but bears can say this is still early, and that if LLMs, wallets, marketplaces, payments platforms or social platforms own more of the discovery and checkout experience, SHOP may have to share more economics or accept lower take rates.”

TTD -7% / RBLX -1.4% / MELI -4.6% more new lows

SOFTWARE

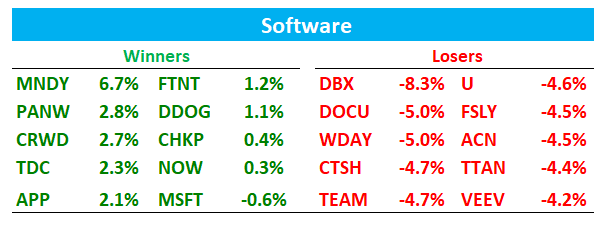

MNDY +6.5% sold off throughout the day after being up 20%+ after the initial print. Bulls liked the big rev and op income beat and said AI producitivity could drive operating leverage, but bears pointed to NDR commentary on the call with mgmt now expecting NDR to slightly decline by year-end as 2024 pricing actions roll off. Here’s the Bull vs. Bear Debate post-print: