TMTB EOD WRAP

QQQs +1.3% on better prints from MSFT and META and ongoing hopes for trade deals and high level contact between DC and Beijing. Yields jumped 5-10bps across the curve of NFP jobs tomorrow as ISM wasn’t as bad as feared (although still bad). Fed expects shifted hawkishly with only 91ps of incremental cuts this year down from close to 105bps yesterday.

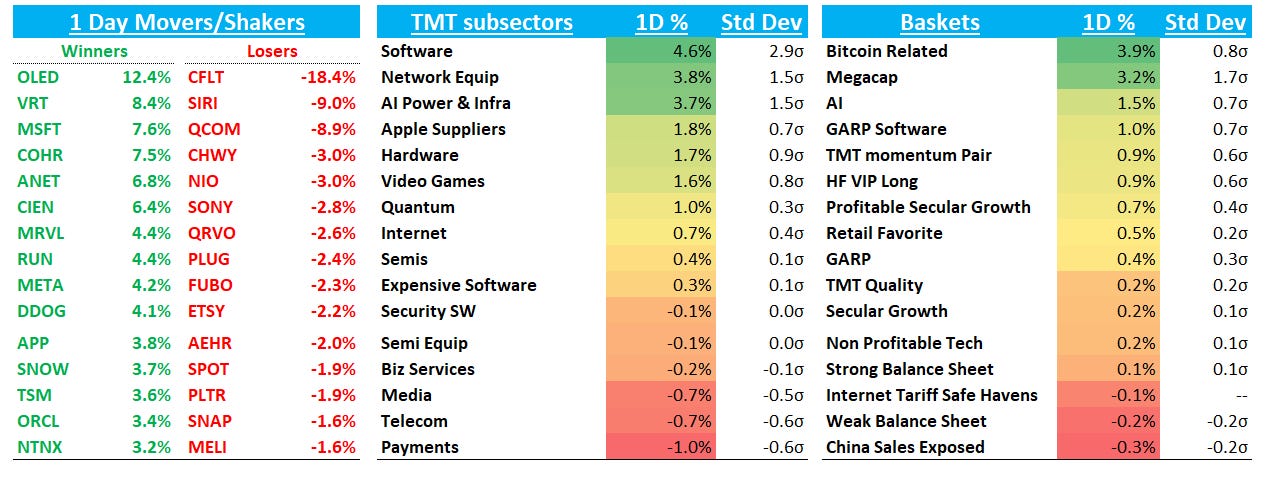

Let’s get straight to the recap (relatively short one today as getting to earnings calls…)

INTERNET

RBLX +3% on a better Q1/Q2 bookings along with a big EBTIDA beat. Mgmt said that strong Q1 trends which reflected the large # of users added in Dec have continued in April, which dovetails with what we have heard from 3rd party data so far. Cowen in their recap note suggested their PCU-based model is suggesting Q2 bookings growth in the 40% y/y range and April engagement data is looking incredibly strong. We found an investors’ quote Jack at JPM passed along to understand the underperformance today: ”: “I hate alt data so much… this is perhaps the most amazing print in TMT and people will just fade it”…Expectations were high and fast money was in the stock. While we pay close attn to 3p data here at TMTB, we try not to game the RBLX quarters and think fast money is missing the transition to a more sustainable 20%+ grower here. We continue to like RBLX’s medium term monetization and secular bull case here: advertising ramp, pricing change driving better bookings growth, increased amount of direct bookings, bringing more content creators to platform, possible Switch 2 integration, AI video game generation driving increased content creation driving flywheel effect, better monetizing in-game / burgeoning partnership with SHOP. 3p continues to point to strong trends so — barring a market pullback — we see no reason why stock shouldn’t be hitting new highs soon along with certain other China/tariff safe haven names.