TMTB EOD Wrap

Good afternoon QQQs -20bps and SPY -40bps. Fed expects shifted in a slightly hawkish direction with market now pricing in 7bps worth of cuts this year as yields popped 6-7bps across the curve following the 5-6% rise in Brent . Stocks were subdued and oil up as some reports out there that violence flare dup in Middle East again for the firs time in weeks, with US and Iran exchanging fire while Iran shot drones and missles at UAE. Trump, for his part, continues to express some optimism for a deal saying Iran negotiators were being “far more malleable.”

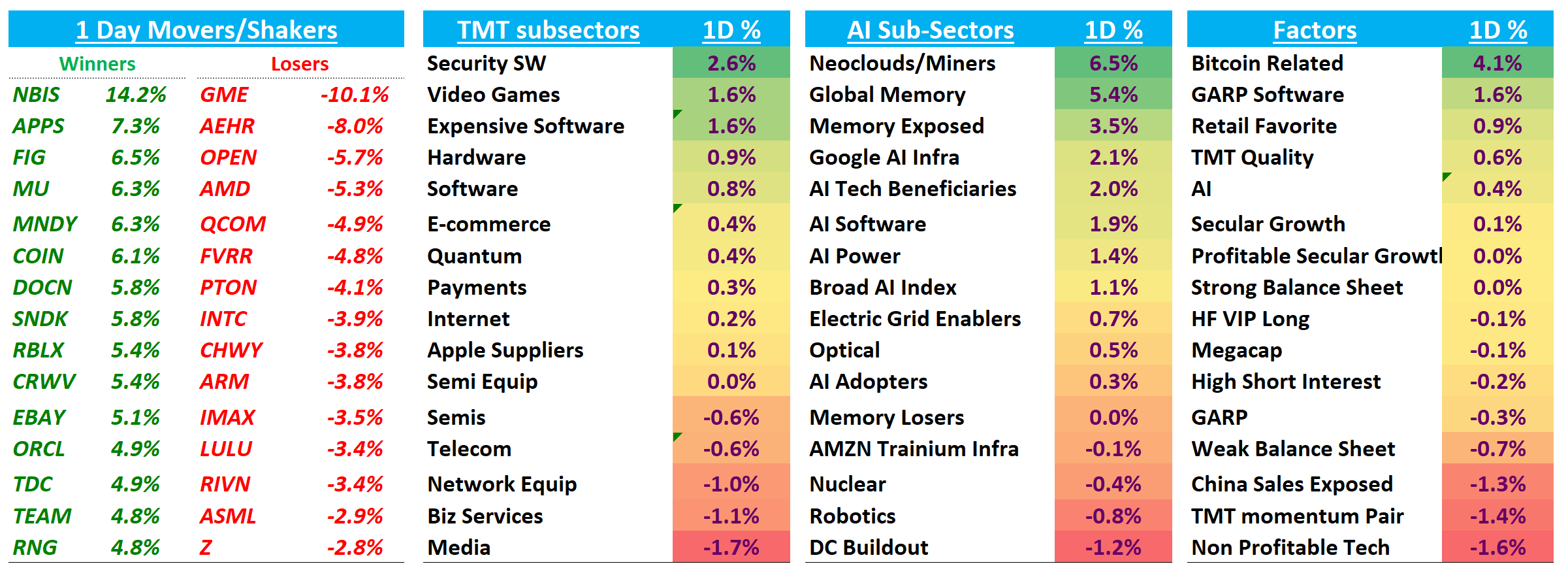

In Tech, neoclouds and memory were the big outperformers today, while software names were large green as software and semis have generally seemed to co-exist somewhat peacefully over the last several weeks without the dramatic factor whiplashes we saw in Q1. Big earnings week again this week which kicks off in earnest tomorrow (PLTR looks ok after the close today but we haven’t gone through it yet - more tomorrow morning)

Lets get to the good stuff…

INTERNET

ABNB -2% on war headlines despite Oppenheimer upgrading to buy arguing new revenue levers (Hotels, RNP/L, AI search) can drive durable acceleration not fully reflected in estimates. Early hotel traction (e.g., Manhattan tests) could add ~3pts to nights with upside if conversion scales, while AI-driven search and sponsored listings improve monetization and mitigate disruption risk (will also benefit from WC Demand). ABNB continues to be one of the names with best sentiment among HFs in internet outside of the hyperscalers. We aren’t involved but sympathize with the bull case and think AI disruption risk is significantly more limited vis-a-vis the OTAs — main push back I hear is valuation given big gap vs. OTAs, but that makes more and more sense in a world where focus is on AI disruption.

GOOGL -63bps as JPM dug into 10-Q (out Friday) highlighting accelerating Paid click growth alongside record query volume. Freedom (?) downgraded to hold as well — no tmuch in the note other than a “take profits” call as note ready pretty positive.

TTD -60bps can’t catch a bid as Wedbush upgraded to Neutral on event tailwinds (world cup/politicl ad spend) saying it will offset competitive pressure in the short term.

SHOP -10bps as M-science was mixed saying GMV trends through April 19th moderating in US while EMEA appears stable. Street already expects a decel.

EBAY +5% as GME put a $56B bid on the table ($125/share). Sell-side out discussing potential tieup with most not completely understanding rationale but noting integration could enhance monetization (take rate & services) and leverage GME’s 4k stores while combining user bases across collectibles, which has been a key driver of EBAY’s GMV as of late.

APP +3% as edgew was mainly positive saying feedback encouraging with share of UA/inventory rising, although they point out there is less momentum vs 2023-2025, and seeing CloudX as more a 2H competitive threat. FundaAI was also positive with some checks saying strong Q1 driven by gaming (aided by Apple Link-out and improved AI bid shading) and a first-time CTV contribution, though e-commerce dipped ~11% QoQ due to post-Black Friday pullback, but they called out e-comm accelerating in Q2 behind algo impreovements and self-service adoption ramp. Jefferies and BofA were also out positive with some checks: Jefferies cited survey data showing APP gaining share (+115bps in ’26) and remaining a top-3 DTC e-comm channel (ahead of TikTok for existing customers), with new products (Discovery, GenAI video) supporting upcoming e-comm launch. BofA highlighted accelerated Axon pixel adoption though pointed out referral cohort spend trends were mixed.