TMTB EOD Wrap

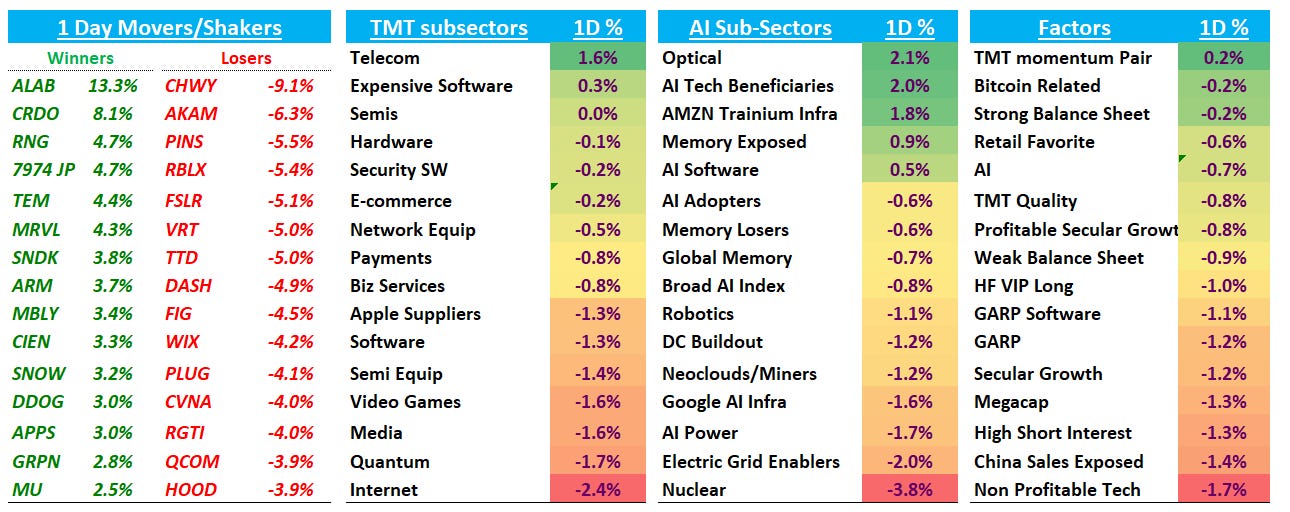

Good afternoon. QQQs -60bps on a day that that Mizuho aptly called “unwind of an unwind.” The early morning started with software and internet rallying strongly at the expense of semis, which were down 3% at one point while software was up 1%+. The day finished with semis +1% and software -1% as the software rally fizzled out. TMT Mo was down 7%+ again at one point for a peak to trough decline of 20%+ before putting in a hammer and finishing flat on the day.

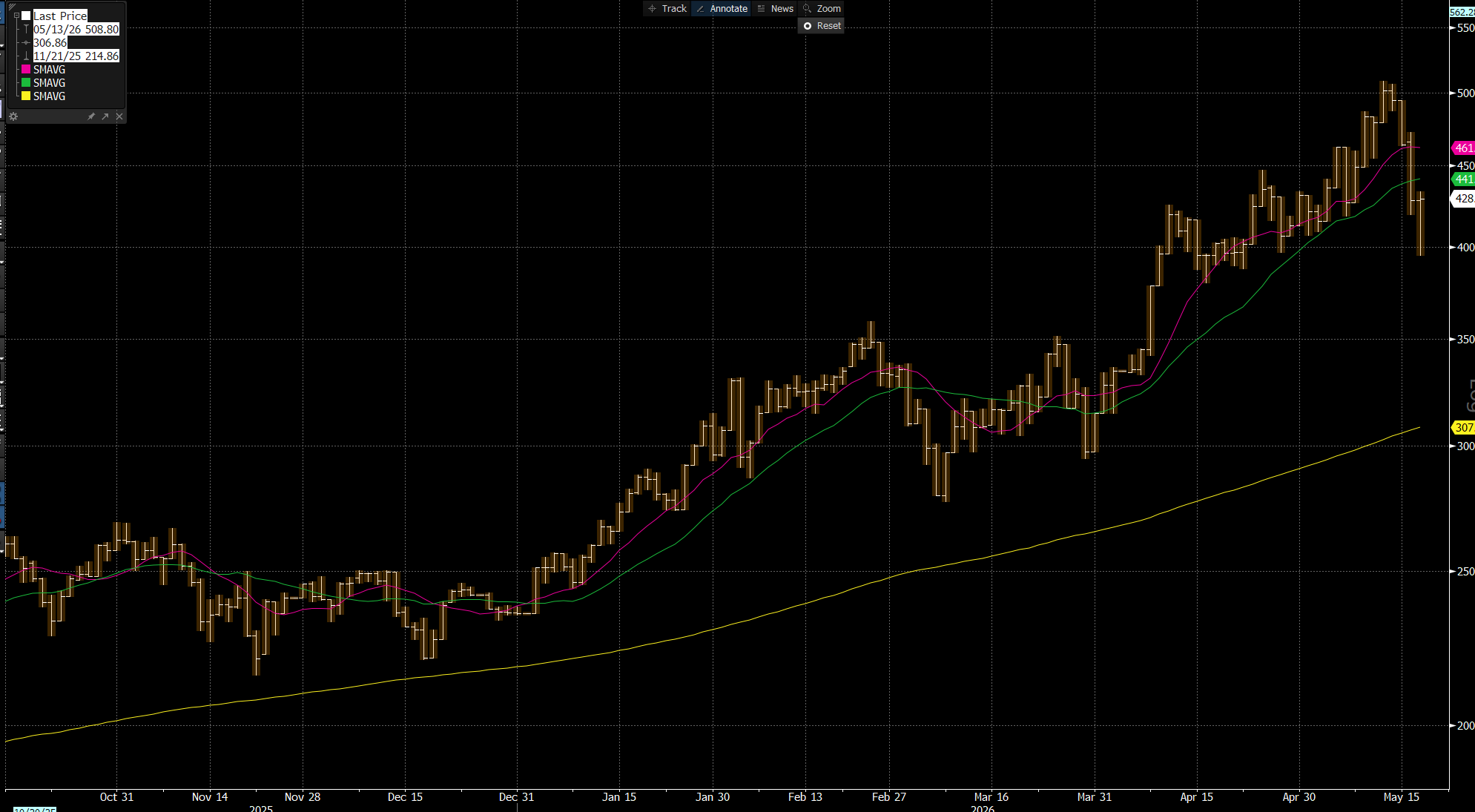

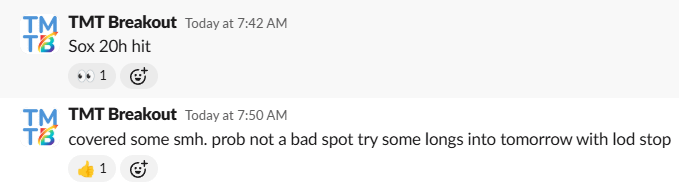

What caused the reversal? No big news came out — we think largely factor see saw and technical as SOX hit the 20d, which we had expected. This weekend we wrote how we expected an early week decline into the 20d before a bounce and we flagged the hit in TMTB Slack early morning:

We trimmed some off that trade but expect the 10d to be hit from the underside before or right after NVDA. Right now, our base case continues to be some chop near-term as rates, hawkishly shifting Fed expectations, and Iran have put somewhat of a damper on the AI semis animal spirits (more of a breather — AI trade still feels very much intact but macro headwinds bear watching). That means we’re being more tactical than normal in our short- and medium-term books. Generally, we’re not hearing investors aggressively add gross or trim yet despite the pull back — a lot of wait-and-see with investors re-evaluating where the best place to put money to work is. We remain on our toes and on the lookout for tea leaves.

On the macro front, things still remain wobbly. Oil was flat, but investors have their eyes on yields, which rose another 6-9bps across the curve while fed rate expectations have shifted to 80% chances of a hike by the end of the year. The 30 year is hitting highs not seen since the 2007. 10 year now at 4.67% and question is how long will rates continue to rise and how far. The glass half full is that we saw real money buying in 2023/2024 when rates hit up against the 4.8-5% levels. Glass half empty is that — and I saw Citrini make this argument — the “AI capex is a double edged sword” meaning that the economy can now withstand a lot more given AI investment driving GDP, but that also means rates could stay higher before recession fears put a bid under bonds.

Let’s get to the good stuff…

AI/SEMIS

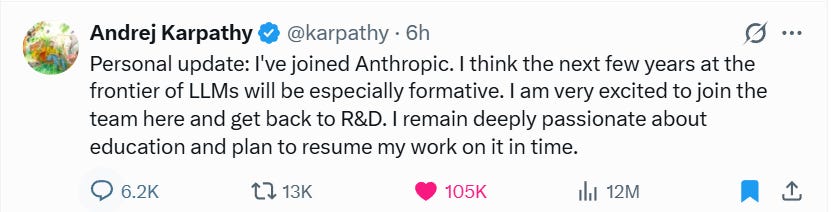

Hearing he got $100M pre-IPO series H sign on. Good get for the Anthropic team.

Trainium names led the way higher today led by ALAB +13%, CRDO +8%, and MRVL +4% catalyzed by a TheInformation article which had a lot of positive snippets around customers wanting to use Trainium:

Anthropic and OpenAI, which have struck multibillion-dollar investment and infrastructure deals with Amazon, have already committed to renting large amounts of current and future Trainium capacity. Now, recent software improvements are prompting smaller developers to consider moving more workloads to Trainium, half a dozen people who use or work with the chips said.

The Trainium theme has gained steam over the last few weeks and Gavin Baker added some fuel to the trade with his comments at Sohn. We flagged it in our weekly on Sunday: