TMTB EOD Wrap

QQQs +1.5% to new closing highs as risk-on the name of the day with Middle-east tensions and a measured message from Fed Chair Powell revived risk appetite. Bulls remain firmly in control Yields fell 4-6bps across the curve. Crude down 5% as the energy trade slipped helping the bid to QQQs. BTC +2%. The market is now pricing in 60bps of incremental cuts this year with next cut set to arrive in Sept.

In Tech, SOX +4% led the way higher as semis looks to break out of a year long consolidation as many names were up 3%+:

Software and Internet strong too with plenty of big moves. From a factor lens, non-profitable tech led the way higher while TMT mo lagged…

Let’s get to it…

INTERNET

DUOL -6% has been a nice short in a bull market, now -20% since we wrote it about it last month as 3p data continues to track lower for both paid net adds and bookings. Lower magnitude beats on a high multiple stocks usually = a good short. Also some burgeoning AI headwinds here as LLMs improve and glasses take off, improving real time language translation.

Ad names strong today - sell side checks generally positive over the last month and easing geo-political tensions helped: SNAP +5%; PINS +5%

RDDT +5% and +2% in the post as hearing Clev initiated positive calling out top line upside in next 1-2 years and strong ad checks. Today, Citi raised PT on ad momentum after positive meetings with mgmt at Cannes, who highlighted RDDT finally leverage its data corpus through RDDT answers and Community Intelligence dashboard. They also said CMOs told them that Gen Z and Y are beginning searches directly on RDDT, one reason they see traffic stabilizing and improving. RBC also highlighted two emerging positives: growing content in-flows as brands shift strategy in response to LLM-driven SEO disruption, and Reddit's crackdown on multiple IP logins, which could modestly lift logged-in user metrics…Clev also initiated with a Buy post-market - hearing they said they see significant upside over next 1-2 years.

META +2% as Citi said META was standout in their checks — they raised #s and kept as top pick.

GOOGL +1% continues to lag other large cap despite Citi saying GOOGL search surprised on the upside and most advertisers still see it as the highest ROAS channel.

TTD +4.3% as Citi noted retail media/CTV upside despite continued AMZN concerns

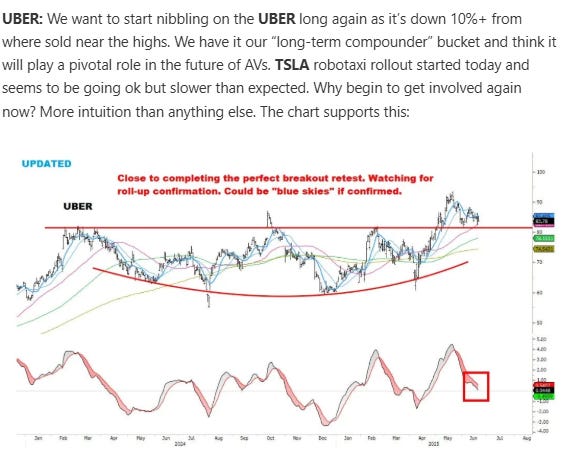

UBER +7.5% as some negative press regarding TSLA’s robotaxi launch, such as cars driving in lanes they shouldn’t be driving in. Also launched Waymo in Atlanta today. Here’s what we wrote in our weekly on Sunday (chart from MacroCharts):

Travel strong: BKNG +3%; EXPE +2%; ABNB +1.2%

ROKU +3.5% as Googl cut smart TV budget

SEMIS

AI names strong across the board. Jefferies recapped their month-long swing through Asia which left Connor (analyst) more constructive on the AI infra cycle, lifting his ‘25/’26 BW rack forecast after checks with SMCI and other OEMs showed a smoother GB300 transition and a 3x jump in monthly rack output beginning in Q3. He called out sovereign AI as the big incremental theme, saying 5 recently announced gov’t back campuses alone imply $180B of NVDA revenue. NVDA +2.6%

AMD +7% nice follow through on yesterday’s upgrade as investors look to get back into AI laggards (remember AMD, DELL. MU were all darlings back in ‘23/’24 and all coming back into vogue - we’ll know we are at the end of the roadwouldn’t be surprised if even SMCI gets a bid at some pt!). Investors generally getting more excited about 2H of AMD, Mi400 launch next year, and sovereign demand which also helps them.

AVGO +4% to new ATHs - that dip was short and sweet as stock got upgraded at HSBC today. The firm raised its FY26/FY27 ASIC revenue estimates by 58%/96% to $28.4B/$42.8B—now 42%/69% above consensus—as hyperscaler ASIC capex allocation is projected to grow from 2% in FY23 to 14% in FY27e. HSBC also expects ASPs to rise sharply, forecasting 92% y/y growth in FY26e and 25% in FY27e on larger die sizes.

MU +4.8% continues to rip as asia press continues to call out DRAM prices going bonkers. I don’t think old time semi investors have seen what’s going on now - secular + cyclical coming together perfectly and playing off each other: As capacity being shifted to HBM (demand forecasts too low), DRAM prices sky rocketing at the same time. That argues for a higher peak multiple than investors have gotten used to on a name like MU. 13x $15 = ~$200. Hynix already breaking out to new ATHs in Korea.

Other AI names: CLS +5%; VRT +5%; MRVL +5%; ARM +4.4%

NXPI +4% as MS was out bullish

SOFTWARE

Cyber names lagged as geopolitical tensions eased: CHKP -2%; CRWD -1.3%; PANW -80bps; ZS -60bps

What didn’t lag? PLTR +2.4%, which to me tells me stock wants higher. Riding the 20d, moving up the stop to breakout level.

SNOW +4.4% as MS initiated at Buy with $262PT calling out a $300B AI/Data opportunity

MSFT +85bps lagged as more news begins to drip out of increasing competition between them and OpenAI

GTLB +5%: Bears continue to argue AI-first tools like Cursor are shifting development paradigms, but bulls will say GitLab’s suite-led approach, enterprise focus, and compliance positioning remain sticky and at 25% growth and 5x offers value even if growth decels. We’re uninvolved.

Poor ADBE +60bps gets no love as investors remain disintereted.

APP +4.2% getting its groove back - hearing of strong intra-q checks setting — up for another big beat