TMTB EOD Wrap

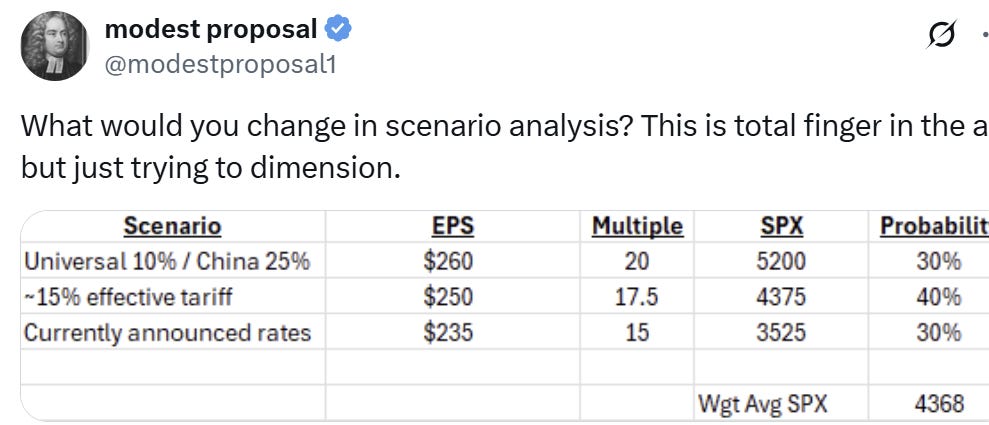

QQQs +24bps with a nice comeback after futures were down close to 5% last night at one point and one of the largest intraday ranges (8%+) since Covid. China dropped 8%. Yields were up 10-20bps across the curve, a big surprise to many - some worries here around higher inflation and a worsening fiscal backdrop + potential for reduced trade deficits to curb demand for U.S. financial assets. Markets continue to price in close to 4 fed cuts this year, down from 4-5 cuts at the beginning of the day. Why the rally? Well didn’t take much to bounce from such oversold levels, especially after VIX crossed 45. News flow continues to point to Trump staying the course although there seems to be more rhetoric around negotiations (ex-China). So far, the narrative/price action seems to squarely point to China-exposed companies being the worst off as most other countries likely to strike some sort of deal (even EU at some point). Good quick back of envelope math below — not saying #s are right, but plug in whatever you see fit…

Let’s get to the recap (excuse typos - trying to get out quick)…

Internet

ROKU +3.3% as Redburn upgraded to Buy saying shift of advertising dollars to connected TV will continue to progress and will likely accelerate if macro headwinds worsen, noting better FCF and EBITDA finally help provide a valuation floor to the stock.

PINS -1.5% as RJ downgraded to Hold from Buy saying they are incrementally cautious given large consumer packaged goods exposure (~15%), which could lead to a sub-seasonal Q2 guide. RJ was also a bit mixed with their latest checks saying mixed vertical performance caused Q1 underperformance and Q2 budget cuts

META +2.2% post releasing llama 4 which got some mixed feedback so far as some called out reasoning and conversational gaps (less fluency than GPT-4o), and less multimodal capabilities vs GPT-4o & DeepSeek V3 although 10M context window pretty stellar. Tiktok deal also put on hold after China / Trump Tariff spat — uncertainty on this front good for META. RJ was also out with some positive checks saying strong Adv+ performance is helping maintain resilient ad spend. Reminder, lost in all the market vol last week,

DASH +2% as BofA said online delivery resilient to inflation and recession as their checks how Q1 acceleration and resistance to menu price inflation (their cc data showed online restaurant as 2nd highest growth category). BofA noted that during inflationary periods, DASH maintains steady order volumes with same frequency but fewer items per order and shoud benefit from improved labor supply in case a slowdown should occur. 3p continues to track 1-2ppts above street for GOV growth.

SPOT +3% / NFLX +1.4% hideouts as not affected by tariffs

RDDT +7% as Truist initiated with a buy and RJ had some encouraging checks.

SNAP -4% as RJ said Sponsored Snaps monetization going well but mixed DAU growth and limited scale mae them less well positoiniend vs. META/AMZN in a downturn

AMZN +2.5% will likely see some pulled forward demand before tariffs take effect

Travel weak on chart below: ABNB -30bps; BKNG -1%; EXPE -1.5%

GOOGL +80bps in front of Cloud Next begins on Wednesday

W +5% despite the Citi downgrade to neutral / CVNA +3% after massive sell off last couple of days

EBAY -2% as stock remains one of best positioned in internet for tariffs (limited exposure), downturn (consumers go to ebay for lower prices), and potentially inflation as higher ASPs should drive better margins/revs. However, given stock outperformance will likely underperform on days like today

China weak: BABA -9%; PDD -4%; BIDU -3%; FXI -8%

Semis

AI trade helped by some positive news flow over the weekend and this morning. Hon Hai said revs +24%, fastest growth since 2022 on better DC demand