TMTB EOD Wrap

QQQs -3% on a combo on the H20 ban news announced last week and Powell’s speech which was seen as slightly hawkish saying tariffs were “significantly larger than anticipated” which will pressure growth and likely push inflation higher, acknowledging the Fed faces two conflicting elements of their mandate - inflation and growth. WSJ goes into Supreme Court ruling that could affect Fed independence (just add to the list of possible neg left tail risks): “The court is about to take up a question that, while not directly about the Federal Reserve, could determine whether President Trump can fire the Fed chair….But granting the president that power would effectively eviscerate the central bank’s independence by making its seven governors, including the chair, at-will appointees of the president, like the Treasury secretary.”

Yields fell 3-8bps across the curve. Market now pricing in 91bps worth of cuts this year after Fed while Dollar continued plummet, falling 1% to multi year lows. China -3%.

Let’s get to the recap…

Internet

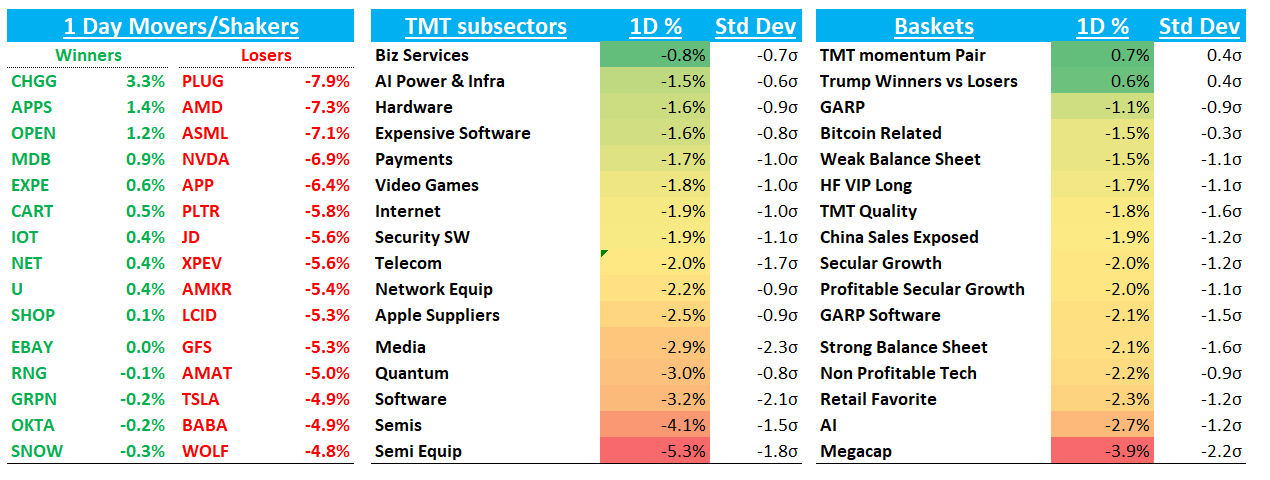

NFLX -1.5%: The discussion here continues to center around the LT guide they leaked ahead of earnings on Thursday. Glass half empty says: why would they leak this in front of a great Q and if its going to be a good q, why schedule an earnings call ahead of a long 3 day weekend. Glass half full: IR team pretty savvy and they know investors would be pissed if they did something like this. In this mkt, LT guide not going to stop stock from going dn on a bad q….We tend to favor the latter although no super strong view here and not sure we will be involved (my bar is a lot higher to be involved when in front of a long weekend). Stock definitely crowded right now…We’ll see what happens Thursday night.

AMZN -3% / META -3.6%: The two biggest losers in internet on my screen - pretty rare to see that. Dynamic at play here is 1) Both are exposed to China/Tariffs/Ads - 3 areas where investors do not want to be exposed to on the long side right now; 2) The more bigger picture theme/regime change of $ flowing out of indexes and headed back to foreign domiciles. Our guy Le Shrub has written a lot on this theme and we agree and think its just getting started and will be a headwind to QQQs for the foreseeable future 3) co. specific reasons: META — FTC trial, weakening ad environment. Temu stopping spend…AMZN — weak cloud checks, tariff/consumer exposure, etc.

Other ad names mixed: RDDT -1%; TTD -1.6%; PINS -2%; ROKU -1.6%. Ad space pretty crowded short at this point among fast money crowd. Our friend Andrew over at Hedgeye who typically does good checks, said today his Agency relationships on SMB side said April was down 30% in ad spend after being up 10-15% for most of Q1 with 2nd week of April stabilizing a bit (-15%)…UBS had a call with Ben Legg who reduced his Q2 forecast to 18% down from 20% (META to 20% down from 25%, AMZN to 21% from 26%)

UBER -1.3% outperformed helped by 1) no China exposure (yes, they get flak for selling their FSD unit, but they also sold Didi) 2) TSLA news around Cybercab shipments stopping 3) that snippet we called out in morning note from BofA about Waymo/Uber possible getting closer ahead of Austin launch

Tariff Safe havens generally outperformed: CART +50bps; RBLX +40bps; CHWY -70bps; SPOT -1.6%