TMTB EOD Wrap

Good afternoon. QQQs +81bps after nice EOD rally. The see-saw continues as the market grapples with different rumors of how exactly the Tariff announcement will look like. Seems like 3 different options: Blanket 20% tariffs, tiered system of three different rates, country by country rates. The bar seems to be 15-20% at this point so anything less than that or tiered by country will likely be met with some sort of initial relief rally. Announcement will take place tomorrow at 4pm. Yields dipped 1-4bps across the curve while Fed expects held steady at 78bps worth of cuts.

IPOs performed well today with Newsmax +180% and CRWV +40% getting back to its IPO range. Another measure of risk on: BTC +3% back to $85k. We’ll see if it means anything but possibly some early tea leaves of where mkt wants to head tomorrow.

Still, economy not great as evidenced by weak ISM (high prices paid) reading this morning and Atlanta Fed GDP taking another leg lower:

Let’s get to the recap…

Internet

RDDT +5% as they rolled out new SMB tools to boost campaign performance allowing advertisers to import campaigns from META Ads manager. SEL:

Campaign Import. Reddit Ads now allows advertisers to import campaigns directly from Meta in just three steps. After signing into their Meta account within Reddit Ads Manager, users can select an ad account and campaign to import, then customize it to fit Reddit’s platform. This seamless process enables advertisers to leverage high-performing Meta ads on Reddit quickly.

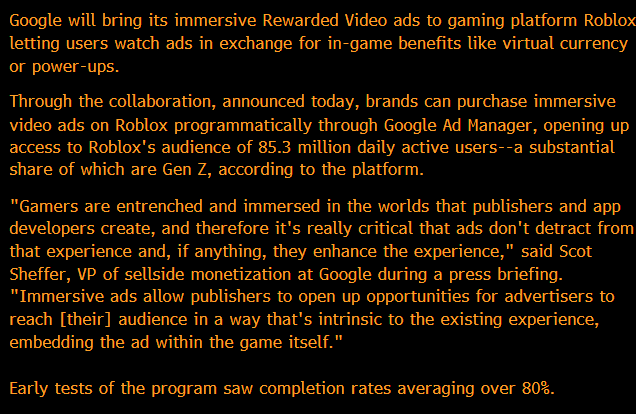

RBLX +4.6% as they announced they were partnering with GOOGL to scale immersive advertising

Wells was positive on the announcement saying they “view Google partnership as a significant milestone in the build-out of Roblox's ad platform, supportive of our ad rev projection of going from ~$100M in '24 to $1B in '27. We believe the Google partnership could meaningfully accelerate Roblox's ad platform adoption by broadening its reach beyond 1P relationships to a greater set of advertisers” and allow RBLX to be more efficient at monetizing.

With 3p bookings and other KPIs tracking well ahead this q + nice secular/structural tailwinds we’ve written about, this one of our favorite longs right now (market notwithstanding).

META +1.6%: New Street had a good note modeling out potential revs for META AI: they said potential revs could be $5B - $54B ($1 - $11 in EPS) by 2030 in their bear and bull cases (base case something closer to $3), calling out AI ad load + a potential subscription.

AMZN +1% as Mizuho called out some weaker near-term checks on AWS and they released Nova Act general purpose AI agent to control a web browser and independently perform some simple actions, and a Nova Act SDK, which will power AMZN’s next gen Alexa+

ROKU +23bps as Wells Fargo made a tactical long idea

TTD +4.4%: Jefferies hosted a call with the founder of Strategists, which manages $40-50M annually saying while TTD remains the "gold standard" for feature functionality and user experience, Amazon’s data advantage and improving DSP capabilities are pulling ad dollars away, especially as campaigns scale more effectively. He also said Google’s DSP is nearing parity with The Trade Desk in CTV capabilities, particularly with upcoming household-level targeting and measurement improvements, while TTD is currently the go to for NFLX inventory (although rumors it might open to AMZN).

Semis

NVDA +1.6%: BAML had a note out after meeting with HonHai yesterday. Said AI server sales up QoQ; sees 30-50K NVL72 racks in 2025...co has started mass production of GB200...HH also said they aren't seeing order push-out to GB300 servers as its clients urge to build computing power as soon as possible due to limited supply. Sounds more positive than the GB200/GB300 news flow we’ve been hearing over the last week. RJ was also out saying no signs of softening and visibility through 2025 sounds good with possible July ramp of GB300, which could benefit Q3/Q4. Opco out saying supply chain positive about GB300 (Ultra) while supply challenges are easing. Back above $110!

Also got continued positive news flow around OpenAI, which like helped AI semis as TheInformation said ChatGPT revs surged 30% in three months:

ChatGPT has hit 20 million paid subscribers, according to a spokesperson. That’s up from 15.5 million at the end of last year, as we previously reported. The strong growth rate suggests ChatGPT is currently generating at least $415 million in revenue per month (a pace of $5 billion a year), up 30% from at least $333 million per month ($4 billion annually) at the end of last year. The actual figure could be somewhat higher, given that corporate ChatGPT plans are more expensive and the company has had early success selling $200-a-month Pro plans, which are 10 times more expensive than basic ChatGPT Plus plans. The overall number of ChatGPT users grew faster than revenue: OpenAI said Monday it has 500 million weekly users, up from 350 million at the end of last year, a growth rate of 43% in three months. It means 4% of users pay a subscription, down from 5% of users three months ago.

AI names: VRT/VST +4%; MU +2% as Citi called out more positive pricing updates from Trendforce; TSM +1.5%; AVGO +1%; MRVL +1.8%

AI networking strong with ALAB/CRDO +4%

Analog names weaker: ON -1.2%; ADI -1.2%; TXN -1%; NXPI flat

INTC -3% as investors a little disappointed Lip-Bu didn’t give out much new yesterday

Software

APP +6.7% trying to get back to its old ways

CRWD +3% as Clev was positive calling out share gains although they also noted lengthening sales cycles in cyber bc of political/macro uncertainty

INTU flat as M-sci said softer IRS volumes QTD

MSFT +1.8% hey now!

NET +2.6% as GS added to conviction list / IBM +70bps as GS removed from conviction list

SNOW +2.3%: GS/ISI/CITI with some positive mentions this morning (see morning wrap)

VEEV -1.6% as MS threw some cold water on the “flight to safety” trade saying while sentiment has improved due to the perception that Veeva's pharma end market offers defensive positioning, the firm sees risk/reward tilted downward with VEEV trading at the high end of its valuation range

HUBS +1.8% as BofA was positive on continued margin expansion

Elsewhere

TSLA +3.5% ahead of deliveries tomorrow as Trump said he expects Musk to eventually return to running his companies. Some neg data from March out of Europe, but what’s new?