TMTB EOD Wrap

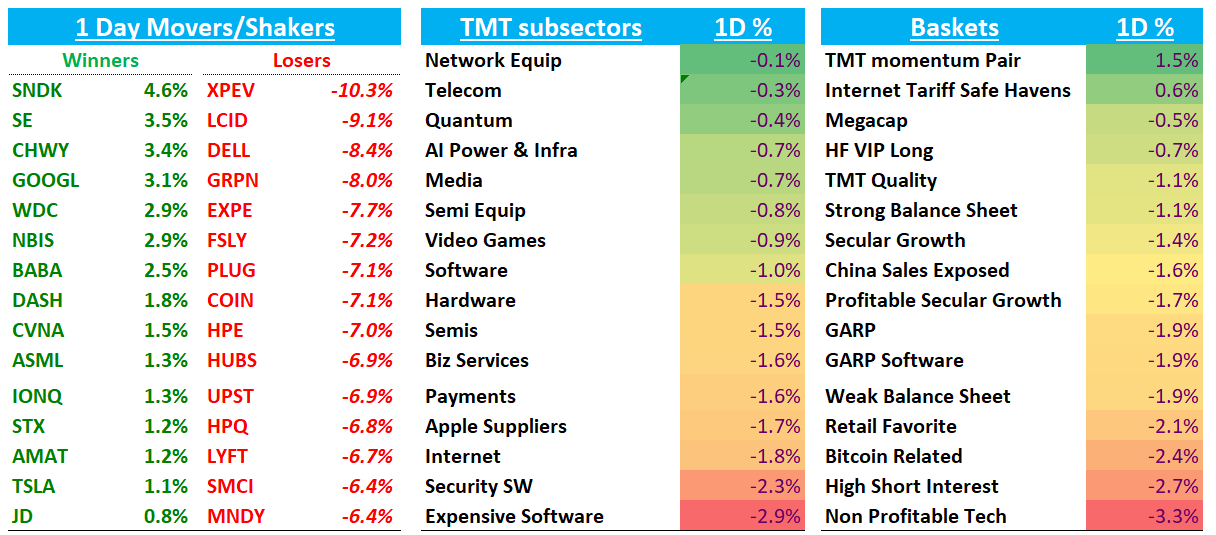

Broad tape generally weaker today with SPY/NDX off 90bps and AI complex lagging with AI leaders and AI semis down roughly 1-2% as a group. On the factor side, crowded longs and momentum bled but so did highly shorted names which points to broad de-risking. The big underperformers were in speculative and rate-sensitive pockets: memes, non-profitable tech, liquid most-short BTC-sensitive all down 2.5-4% as a group. Healthcare and Utilities outperformed.

Just another day in the ASS period: pnl leaking, spreads widening, and a bit of a pain to sit through. In all seriousness, the market is continuing to digest the paradigm shift we discussed over the weekend. We’re still waiting for a clearer narrative/price action picture to emerge.

All eyes in the Tech world continue to be focused on Gemini 3 and NVDA print mid-week. GOOGL exposed AI names outperformed today: AVGO/CLS flat, LITE +4%. Memory and storage names outperformed today (SNDK +4.6%; WDC +3%; STX +1.2%) as Gemini 3 is rumored to have great image gen and video gen. On that note, one thing I forgot to mention in the piece over the weekend is that we’re in the midst of another paradigm shift, which is being highlighted by the Gemini 3 release this week: the likely plateau of chat-bot functionality. The rate of change in improvements in models will likely be increasingly seen in multi-modal like image-gen and video creation, two areas in which having an advantage in token cost will be even more key. Google is the leader here. How does the landscape shift going forward and what does that mean for OAI? Lots of permutations to possibly think about on the Gemini 3 release and potential share shifts will be key to watch — it seems like we did get a bit of a dip in ChatGPT DAUs when nanobanana went viral in early Oct, although it wasn’t sustained.

Again, lots of moves driven by de-risking today and factor shifts today so won’t go into the usual recap, just call out a few interesting movers:

TSLA +1%: Lots of questions on strength today, and we think it is likely attributed this tweet by Gavin Baker, which brought up some things we hadn’t thought about and had us feeling more long-term bullish about Tesla. His basic argument is Tesla’s “low capex” is actually a feature, not a bug: customers fund the bulk of inference capex at the edge while Tesla runs one of the largest, most coherent GPU clusters for training, giving it huge cost-per-token and data advantages in FSD/robotics

Travel names weaker: EXPE -8%; ABNB -3.5%; BKNG -5% as Google rolled out new AI powered travel planning tools inside search/AI model that build full itineraries (flights, hotels, restaurants, events) in one place and will increasingly support direct booking through partners. Despite the blog specifically calling out partnering with OTAs, that raised “here we go again” fears that Google will capture more of the trip-planning surface area and squeeze the online agencies on traffic and ad spend:

“Building a helpful experience for travelers requires deep collaboration with the industry, and we’re already working with partners including booking.com, Choice Hotels International, Expedia, IHG Hotels & Resorts, Marriott International and Wyndham Hotels & Resorts to make this possible. We’re committed to partnering with travel companies of every size so you have all the best options at your fingertips.”

Ad names (META -1%; PINS -4%; RDDT -3%): Digiday had a mixed piece on ad spending. Some key quotes thanks to akhenosiris in the chat: