TMTB EOD Wrap

QQQs +23bps helped by monster RPO/IaaS FY26 guide, which kept the AI vibes going strong. Treasuries rallied and yields fell as we got some dovish data: yields were down 6-8bps across the curve as fed expects shifted back above 50bps worth of cuts for the year. USD -75bps to fresh lows —Trump’s looming potential tariff escalation on July 9th, widening fiscal deficits that could deepen under the reconciliation bill, and Section 899’s extra hurdle to inbound capital—has combined with softer May growth and inflation prints to sap demand for dollars, which is all good for Tech earnings in a little over a month but also points to waning demand for US assets (h/t VK).

Post-close, ADBE looks about in-line as Q2 Digital Media NNARR $460M about inline with bogeys as was Q3 guide. Reiterated FY DM ARR 11% growth. Not really a ton of interest in this name at the moment (including from us) and seems like boring dead money for the time being.

Let’s get to the recap…

INTERNET

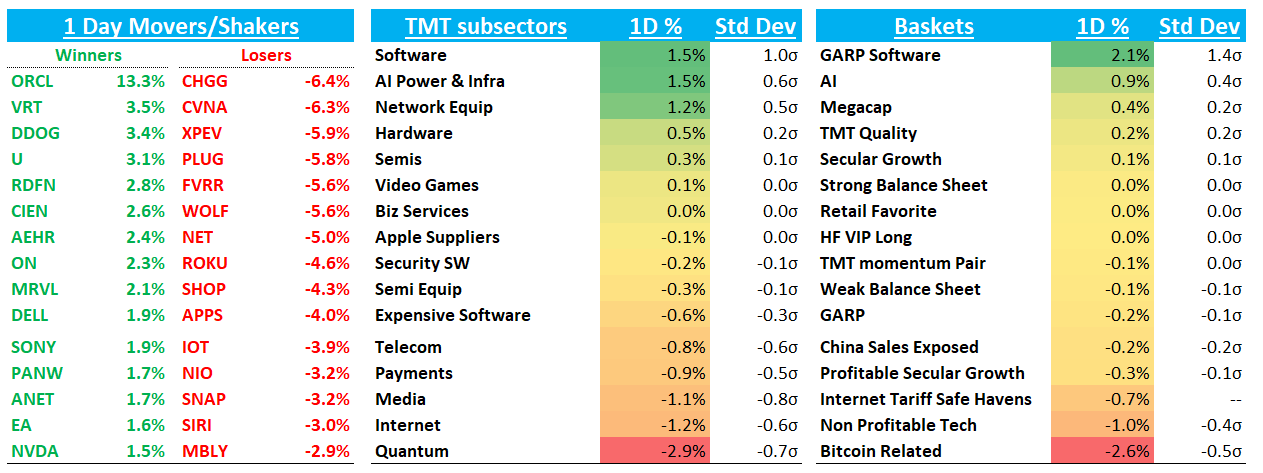

ROKU -4.5% / TTD -2% as Adweek called out doubling of AMZN’s ad load

ETSY -1.5% as Yipit showed a deceleration in the weekly data back into negative territory. The brief sojourn into positive y/y growth was good while it lasted!

CVNA -6% as Chanos was on Bloomberg bashing the stock

CHWY +1% as sell-side defended the big move down yesterday

NFLX -40bps - Yipit said after the close Global net adds trending in line to above street

RDDT +1% some positive price action despite Piper calling out weaker user audience in May. Some good discussion in TMTB chat on the name today.

RBLX -1%: We took some profits on this one today - now down to about ~50% of sizing of what we were previously. Nothing has changed in our medium-term thesis, but chart running into resistance, expectations are high, and we are cognizant Switch 3 sales have been a lot better than expected, which could cause some vol in the 3p engagement data. Just some prudent profit-taking after a very nice run.

LYFT/UBER -1% despite M-sci calling for 1% beat to bookings

Large cap fairly boring day: GOOGL - 1%; AMZN/META flat; NFLX -40bps

SEMIS

AMD -2% after AI day was fairly ho-hum with no huge game changing updates. noting steady progress but no game-changing announcements. AMD highlighted updates on MI350 (in production), MI400 (next year), and MI500 (in 2027), as well as rack-scale and EPYC roadmap detail—but no new major customer wins, which some bulls were hoping for. While AMD is closing the GPU performance gap with NVDA’s Blackwell, the MI450 in 2025 will still be trailing NVDA’s Rubin roadmap. AMD gave no formal revenue guidance but projected the AI accelerator TAM growing to “more than $500B” by 2028 with >80% CAGR.

ANET +1.6% after their AI webinar. ISI gave us a recap of their key takeaways: Ethernet has now caught up with InfiniBand in shipments and is proving more scalable for large XPU clusters, a shift that favors ANET. The firm also highlighted strong interest in ANET’s Linear Pluggable Optics (LPO), which can cut power consumption by 40–50% and ease data center energy constraints. ISI notes software remains a key differentiator, with features like CloudVision providing telemetry, load balancing, and GPU performance insights.

NVDA +1.5% continues to act great and not far away from new ATHs, helped by ORCL’s great print and demand commentary + positive recaps from GTC Paris from the sell-side

AVGO +1.3% dip was short…TSM +1%…Does seem like we are back in early ‘24 market where you just buy the best and cleanest AI semi stories

MU flat as Digitimes said Samsung reportedly failed third NVDA HBM3E test

Power strong: VST +4% / VRT +3.5%

CRDO +3% nice flat after post-earnings pullback