Morning Wrap: Oracle (ORCL) Earnings Takeaways; Tech Research/News

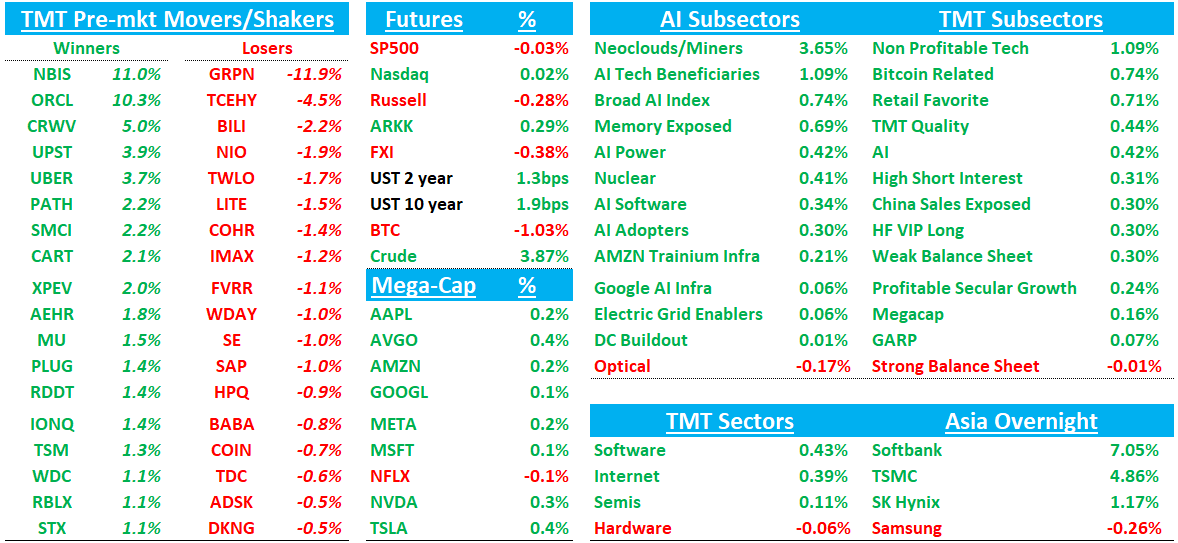

Good morning. Futures up slightly. Oil +4%. BTC -1%. Yields flattish. Asia mixed overnight: TPX +0.94%, NKY +1.43%, Hang Seng -0.24%, HSCEI -0.07%, SHCOMP +0.25%, Shenzhen +0.52%, Taiwan TAIEX +4.1%, Korea KOSPI +1.4%. Nintendo +10% on Pokemon hype. Softbank +7% presumably on the better ORCL #s.

NVDA investing $2B into NBIS +10%

We’ll hit ORCL earnings first then get to the usual.

ORCL: Solid OCI #s, FY27 raise, unchanged FY26 capex guide and much better disclosure around AI demand capacity delivery, funding structure, and profitability.

Overall solid numbers coming in or above bogeys on most key KPIs with OCI accelerating to 84% (81% cc) with the 8 cc handle investors wanted to see. Commentary sounded positive all around, especially around profitability while mgmt also defended the AI is coming for SaaS narrative. Doesn’t solve the longer term debate, but bulls come away content with what they saw this q. Comes on the backdrop of what was obviously negative sentiment and positioning that has been left for dead although heard fast-money was more on the long side heading in give poor r/r on the short side.

The #s:

Revenue was $17.190B, +22% y/y / +18% cc vs Street $16.91B-$16.95B, +~19.7%-20.0% y/y; non-GAAP EPS was $1.79, +21.8% y/y vs Street $1.70-$1.72.

OCI/IaaS $4.888B, +84% y/y / +81% cc, vs Street roughly $4.74B-$4.83B and bogeys of 8 handle cc, while RPO reached $553B, +325% y/y, +$29B q/q, ahead of expects as well

Q4 Guide: Revenue $18.92B-$19.24B, +19%-21% y/y / +18%-20% cc vs Street roughly $19.11B-$19.13B, +~20.1%-20.4% y/y…Cloud revenue growth +46%-50% y/y / +44%-48% cc vs Street roughly +47%-48% y/y

Raised FY27 Revs by $1B to $90B while keeping FY26 capex at $50B, helped by BYOC / prepay structures that appear to reduce incremental funding needs.

Mgmt disclosed 32% gross margin on AI capacity delivered in F3Q, above the prior 30% floor. At the same time, reported non-GAAP gross margin of 65.9% still missed Street, showing the near-term mix drag from lower-margin AI infra revenue and ongoing capacity ramp costs.

Multicloud database revenue grew 531% y/y, cloud database services accelerated to roughly 35%-36% y/y, and ORCL now has global regional coverage across partner clouds, 33 Microsoft regions, 14 Google regions, 8 AWS regions exiting Q3, with 22 AWS regions expected by FQ4 exit. That is a real unlock for migration and could become the higher-margin counterweight to AI infra mix pressure.

Cloud apps grew 11% cc, roughly flat with last quarter. Fusion ERP and NetSuite decelerated some, but deferred revenue still outgrew revenue, and mgmt leaned hard into the view that AI strengthens ORCL’s SaaS moat rather than erodes it (quotes below)

Mgmt explicitly framed ORCL as a likely AI winner in apps, not a victim, and pointed to embedded agents, AI Agent Studio, data gravity, and wins against SAP and Workday.

Color from the callback was generally constructive. The main message was that mgmt said its guidance philosophy has not changed, the new press release / call structure was meant to reduce confusion, and the quarter’s BYOC / prepay deals should be understood as a more asset-light way to serve demand rather than a sign of weaker economics. Mgmt also clarified that BYOC can mean lower TCV than traditional deals, but that profitability is driven more by the strategic value, timing, and location of capacity than by the exact contract form.

Key quotes:

On Saas:

"I don't agree with the thesis that AI will spell the death of SaaS. We've already delivered well over 1,000 agents right inside our horizontal back-office and industry applications, at no additional cost to our customers. Some smaller or single-focused SaaS players may well be disrupted, but Oracle will not be among them. We think AI is disruptive — we do — but we think we're the disruptor because we're actually embedding the AI right into our applications."

"I've not yet met a customer who tells me they're ready to give away their retail merchandising systems, their core banking systems, their electronic health record systems because some small cobbling together of niche AI features is going to replace all of that overnight. What they're asking is, how can we consume as much AI out-of-the-box that you're putting into your applications as quickly as possible?"

On capacity:

Through our partners, we have secured more than 10 gigawatts of power and data center capacity coming online over the next three years, and greater than 90% of that capacity is fully-funded through our partners. We have tripled our manufacturing sites and increased rack output by 4x all in the last year. Time from rack delivery to revenue has reduced by 60% in the past several months. In Q3, we delivered more than 400 megawatts to customers, and 90% of that committed capacity was delivered on or ahead of schedule."

On Profitability

“Looking at the AI capacity we delivered in Q3, our gross margin for that remained above our 30% guidance at 32%. Now combine that with our other segments of OCI, which have much higher margins, like our Database Services, and you can see why Oracle is growing so quickly and profitably.

"When you think about the overall profitability of these AI data centers, we gave guidance of a gross margin in the 30% to 40% range on the accelerators themselves — that continues to hold and we see it continuing to incrementally improve. The other thing to understand is that in these AI data centers, typically on the order of 10% to 20% of the total spend is going to adjacent services which have higher margins. And our Multicloud Database business is a much higher margin business, more in the 60% to 80% range, growing very rapidly. When you combine all of these pieces together, the overall margin profile of OCI continues to strengthen."

"The limitation on profitability is not on the capacity we've delivered — that one is profitable. The reason we're not even more profitable right now, despite continuing to grow EPS, is because we have so much under-construction at one time.

Bull vs. Bear Debate

Bulls say ORCL is crossing the line from “promised AI winner” to “proving AI winner.” Before this quarter, a lot of the story rested on huge RPO disclosures and long-dated targets, but investors had legitimate questions about whether ORCL could actually deliver capacity on time, whether customers would stay committed, and whether the economics would justify the capex. F3Q moved those questions in the right direction. OCI accelerated from +66% cc to +81% cc, AI infra grew 243% y/y, multicloud database grew 531% y/y, and ORCL delivered 400MW while saying 90% of committed capacity was delivered on or ahead of schedule. The FY27 revenue guide also moved up again, to $90B, which suggests backlog visibility is improving rather than deteriorating.

Bulls also think the market is still underestimating how much of the ORCL story is no longer just GPU rental. The more durable and higher-quality part may end up being the combination of multicloud database, database services, adjacent OCI services, sovereign cloud / Alloy, and AI-infused applications. That is why the halo effect matters. Mgmt is saying AI infrastructure is pulling through database migrations, larger app conversations, and more sovereign / dedicated-region demand. If that is right, ORCL is not just a capex-heavy infra story; it is becoming a broader full-stack platform story with higher-margin layers riding on top of the AI infra build. On valuation and growth, bulls can reasonably argue that ORCL can do ~34% revenue growth in FY27, then stay above 20% beyond that as OCI, multicloud DB, and sovereign / Alloy burn through backlog. If EPS can move toward roughly $10-$12 over the next couple of years, and if the longer-term path toward something like $16+ remains credible in FY29, then a 20x+ P/E discounted back can get a $250+ stock