EOD Wrap: SaaSpocalypse v.13; Memory vs. HPE/DELL; ARM $25B / $9 within 5 years

Good afternoon. QQQs -70bps after a late day swoon as SOX +1.3% one of few areas that were green in Tech. Treasuries continue to see selling pressure, with yields rising 4-7bps across the curve. BTC -3%….however, as I’m writing this futures +1% as there is chatter of ceasefire. Unclear how real it is…

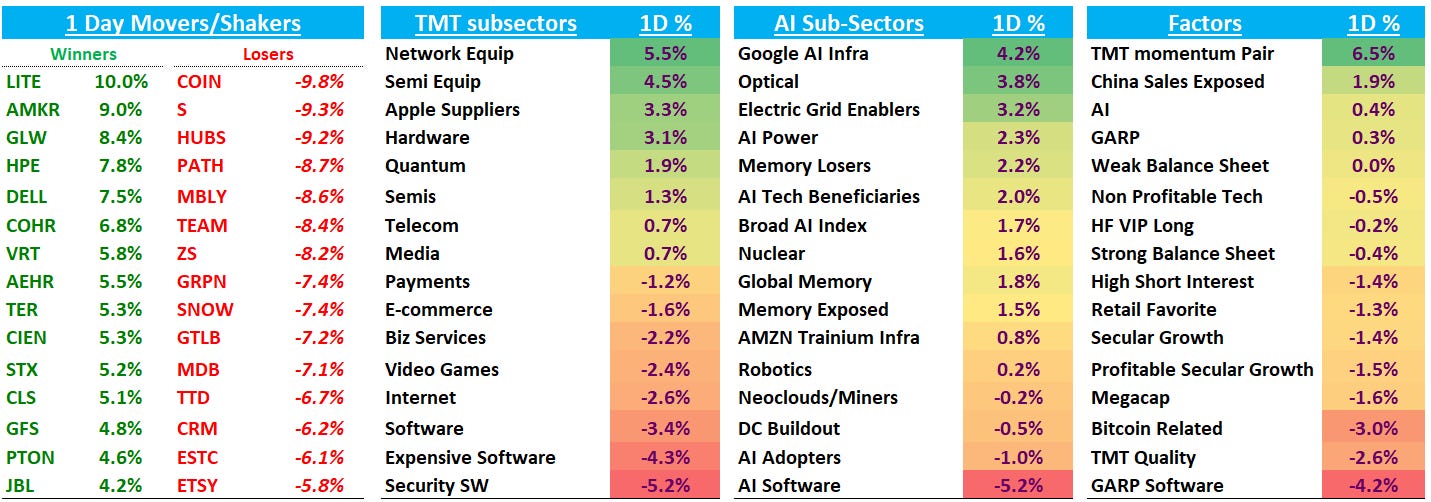

Main story in Tech today was Semis outperforming software by 470bps+, with optical/networking leading the way higher and helping TMT Mo Pair key in on a +6.5% day. Here’s the GS TMT Mo L vs. S basket (early March drawdown was short and sweet):

IGV/SOX ratio now down 13% from its peak back in the first week of April:

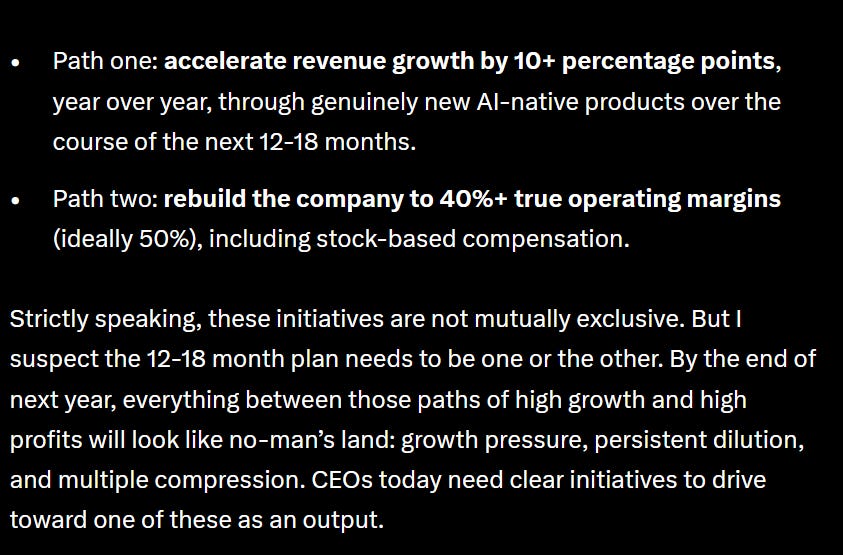

Why the underperformance in software today? A confluence of things.

First, we all know that token growth/demand continues unabated so AI semis a relatively safe place to hide in terms of macro weakness. Second, Anthropic announced a new feature that allows Claude Code and Cowork to control your computer - out on MacOS and shortly on windows. Call it an OpenClaw competitor that just further fanned fears of sw obsolescence. Third, TheInformation reported AMZN is cutting AWS staff as they get better at automating functions in its sales, business development and other groups, raising fears of seat compression. Fourth a16z had a fairly negative piece on software, saying there are only two paths for SaaS CEOs:

Finally, some pointing to a negative note out by Cleveland on Team, saying outlook is mixed with partners saying changes could mean a flat to down year while competition also picking up. Then you had the SAP downgrade by JPM who had been a big bull on the stock citing two structural concerns: a potential shift toward consumption-based revenue (CEO Klein increasingly signaling this) that could introduce volatility and pressure gross margins, and intensifying AI competition forcing higher investment spend. This comes on the back of Cleveland’s SAP downgrade a couple of days ago.

Just one thing on top of the other today.

Near the close, WSJ reporting that OpenAI winding down Sora:

CEO Sam Altman announced the changes to staff on Tuesday, writing that the company would wind down products that use its video models. In addition to the consumer app, OpenAI is also discontinuing a version of Sora for developers and won’t support video functionality inside ChatGPT, either.

Here’s TheInformation with a little more insight:

"At the same time, he said the company had completed the initial development of its next major AI model, codenamed Spud, and would wind down the Sora AI video mobile app, which employees had complained was a drag on the company’s computing resources during a time of heightened competition with foes such as Anthropic and Google."

Looks like its GOOG & META’s game now…

ARM (+7% post-close) also out post close with CEO on bloomberg putting out a $25B / $9 EPS target within 5 year. Street is at $13.3B / $5 in CY 2030 and $7 / $18B in 2031 fwiw…calling out $15B from new AGI CPU chip which will have as many as 136 cores.

Let’s get to it…

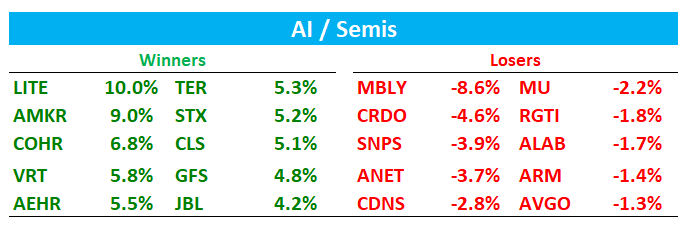

AI / SEMIS

A bit of unwind in the memory trade as MU -2.2% / SNDK flat and HPE +7.5% / DELL +7% (DRAM has been a big headwind for the latter 2). As we wrote yesterday, DRAM spot prices rolling over a tad (even though contract prices for DDR5 continue to hold up). The news around SK Hynix accelerating supply/ higher ASML EUV orders didn’t help. Both HPE and DELL also helped by SMCI’s legal woes where they are unlikely to get allocation from Jensen they would have previously got, which means more share gains for DELL/HPE. I was going to write about HPE this upcoming weekend, but market waits for no one. The quick elevator pitch: